2018 Net Lease Retail Sales Volume & Cap Rates

Single-tenant retail sales volume versus average cap rates, updated quarterly.

Source: Stan Johnson Co. Research, Real Capital Analytics

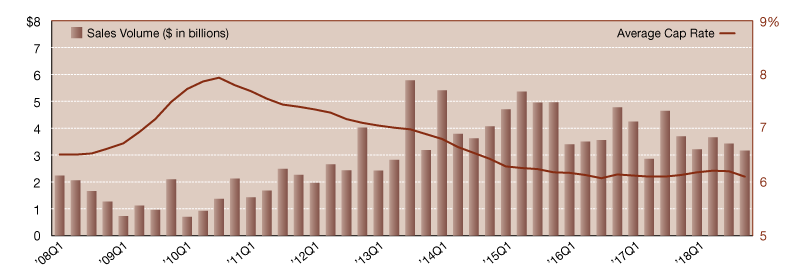

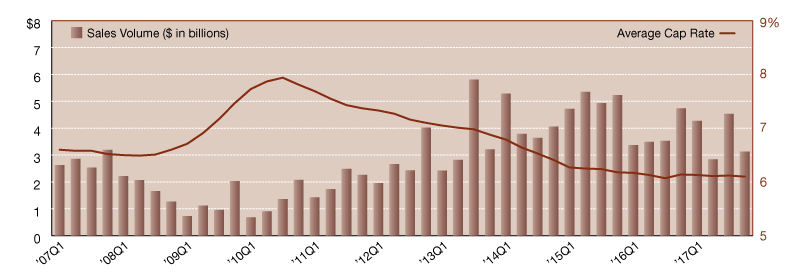

Despite the overall single-tenant market ending the year with a significant amount of sales volume, the retail sector lagged. With only $3.2 billion in sales, fourth quarter 2018 reported the lowest quarterly volume in the last 18 months. Annual sales totals, nearing $13.5 billion, were also lower than average in 2018, and yearly retail sales were the lowest reported since 2012. Cap rates declined for the second consecutive quarter, falling nine basis points to 6.11 percent. This downward movement should not suggest a future trend, however. With lower sales volumes and lower cap rates, it is likely that a gap in buyer/seller expectation is impacting current trends. When premium properties are the only ones trading in a shifting market, sold cap rate averages may not yet reflect the increases we’re seeing in today’s asking cap rates. In future quarters, cap rates are expected to inch upward, although sustained increases are not likely until late in 2019. As buyers and sellers adjust to changing market conditions, single-tenant retail sales totals are also expected to climb, providing the overall market maintains its currently strong appetite for investment.

Focusing on business development, industry and client-specific research, and the analysis of local and national market trends, Lanie Beck has been the Director of Research for Stan Johnson Co. since 2013.

—Posted on Feb. 13, 2019

Source: Stan Johnson Co. Research, Real Capital Analytics

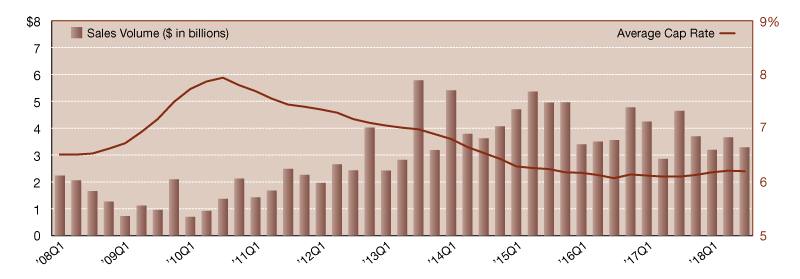

After reporting a record high annual total of nearly $20.0 billion in sales during 2015, the single-tenant retail sector fell back in line with average totals the next two years, reporting more than $15.0 billion in annual activity in 2016 and 2017. Unfortunately, at only $10.1 billion year-to-date 2018, the retail sector is not on pace to match sales volumes reported in recent years. With quarterly averages only ranging between $3.1 and less than $3.7 billion this year, the final quarter of 2018 is not likely to have enough momentum to push sales much past the $12.0 to $13.0 billion range. Average cap rates stayed essentially flat in third quarter, reporting a one basis point decrease to 6.20 percent. With very minimal movement in both directions over the last few quarters, the single-tenant retail sector continues to display signs of the “U”-shaped trendline, as cap rates have bottomed out but have yet to show much growth. Noticeable and sustained upward movement will likely not occur until sometime in late 2019, although increasing interest rates could certainly impact this trend more quickly.

Focusing on business development, industry and client-specific research, and the analysis of local and national market trends, Lanie Beck has been the Director of Research for Stan Johnson Co. since 2013.

—Posted on Nov. 12, 2018

Source: Stan Johnson Co. Research, Real Capital Analytics

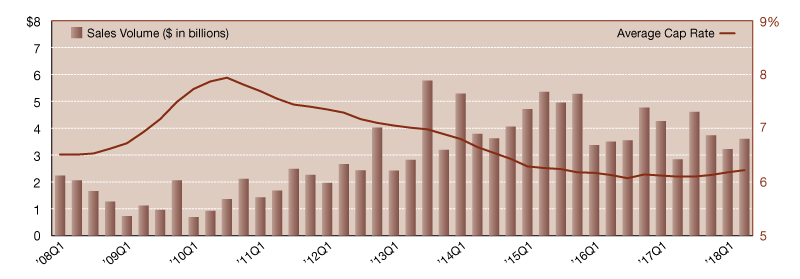

The single-tenant retail sector reported quarter-over-quarter increases in sales volume, logging $3.6 billion in sales during second quarter 2018. This brings the year-to-date total to just shy of $7 billion, putting the sector on track to narrowly miss annual totals reported in the last two years. Average cap rates in the single-tenant retail sector increased for the third consecutive quarter, ending mid-year at 6.2 percent. This is the highest average cap rate reported since third quarter 2015, and trends indicate the market should expect to see a continued rise in subsequent quarters. Retail sales continue to be dominated by private buyers, and at mid-year, 67 percent of all single-tenant retail transactions involved a private buyer. This percentage is up slightly from figures reported in 2017, but equal to private buyer activity reported in 2016, when institutional buyers started to pull back.

Focusing on business development, industry and client-specific research, and the analysis of local and national market trends, Lanie Beck has been the Director of Research for Stan Johnson Co. since 2013.

—Posted on Aug. 15, 2018

Source: Stan Johnson Co. Research, Real Capital Analytics

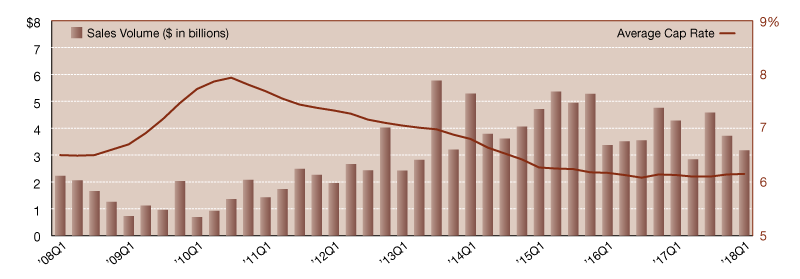

The single-tenant retail sector saw sales volume dip in first quarter 2018. Down 25.7 percent from the same period last year, less than $3.2 billion was reported in the first three months of 2018. Compared to the other asset classes, retail outpaced the $2.8 billion reported in the office sector, while the industrial sector contributed nearly half of the quarter’s total volume with almost $5.3 billion in sales. Single-tenant retail continued to boast the lowest cap rates across the market, with an average of 6.2 percent. Rates have been fluctuating only slightly over the last two years, and despite a single basis point increase in the last three months, there has been no discernable or sustained uptick quite yet. Retail sales in first quarter were dominated by private buyers–71 percent of all retail transactions included a private buyer, and while they have been the predominate buyer type in recent years, we saw public REITs pull back and domestic institutional buyers give up market share in the early months of the year.

Focusing on business development, industry and client-specific research, and the analysis of local and national market trends, Lanie Beck has been the Director of Research for Stan Johnson Co. since 2013.

—Posted on May 15, 2018

Source: Stan Johnson Co. Research, Real Capital Analytics

The last two years have seen a single-tenant retail market in flux. Sales volumes have been see-sawing between much higher than average totals–in Q1 and Q3 2017, for example–and some of the lowest volume quarters on record in the last five years–Q2 and Q4 2017. Despite the fluctuation, the retail sector managed to report respectable sales volume totals for the year, reporting $14.8 billion. Despite it being the lowest annual total since 2013, we do not expect to see this downward trend continue. Instead, sales should rebound in 2018 as pent up demand drives transaction volume this year. Average cap rates in the single-tenant retail sector have essentially bottomed out. After reaching a low point of 6.1 percent in Q3 2016, the following five quarters have seen rates inch up and down insignificantly. By year-end 2018, we expect to see average retail cap rates noticeably moving in an upward trajectory.

Focusing on business development, industry and client-specific research, and the analysis of local and national market trends, Lanie Beck has been the Director of Research for Stan Johnson Co. since 2013.

—Posted on Feb. 21, 2018

You must be logged in to post a comment.