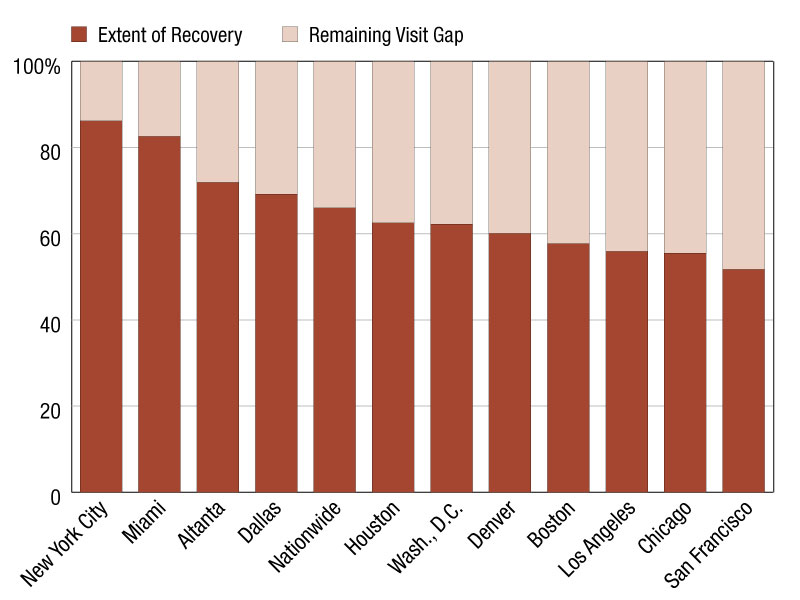

Challenges Face Retail Real Estate Through Year-End 2010

Although Moody's does not expect investment-grade retail REITs to see any material changes to their current ratings and rating outlooks, non-investment grade retail REITs' ratings may be pressured. Moody's has a stable outlook on the majority of its rated retail REITs, but maintains a negative outlook on the overall real estate fundamentals of the retail REIT sector.

By Merrie S. Frankel, Vice President & Senior Credit Officer, Moody’s Investors Service – Commercial Real Estate

Retail real estate fundamentals will be challenged for the next year.

Although Moody’s does not expect investment-grade retail REITs to see any material changes to their current ratings and rating outlooks, non-investment grade retail REITs’ ratings may be pressured. Moody’s has a stable outlook on the majority of its rated retail REITs, but maintains a negative outlook on the overall real estate fundamentals of the retail REIT sector.

Retail industry executives share some of the same mixed view. For example, at the ICSC conference in Las Vegas last month, the pervading sentiment was that the retail real estate industry had reached an inflection point, with executives feeling “cautiously optimistic.”

During the past year, retailers closed stores, reduced inventories and cut staffs, negotiated lower rents and increased concessions, while consumers curtailed spending and increased savings. High unemployment, low-disposable income, and a protracted economic downturn continue to challenge credit conditions for retailers.

Despite relatively long-term leases with retail tenants and solid coverages, many REITs are still experiencing decreasing or negative rent-spreads, as well as occupancy, collections and returns below historical norms. Leasing has picked up for most REITs, but tenants have negotiating leverage and are opening stores in a measured fashion as they exploit a unique opportunity to capture attractive stores in quality locations.

Consumer confidence is starting to rise and retailers have become healthier companies that are better equipped to navigate the current environment, but we anticipate real estate fundamentals will remain pressured for at least the next year due to the lagging nature of retail real estate. In addition, the sovereign debt problems in Europe could negatively impact the nascent economic recovery in the United States, creating a further drag on retail REIT performance.

On the plus side, many retail REITs have relatively stable leverage, large unencumbered portfolios, and reduced liquidity issues due to robust unsecured debt and equity issuances. In addition, retail REITs have implemented cost containment strategies, severed development pipelines, and exhibited astute balance sheet management. Fresh retail concepts are also spurring new store openings.

Aside from consumer sentiment, challenges include consolidation, store closings, and retailer bankruptcies, which continue to negatively impact credit quality and the ability to push rents. There is, therefore, a greater bifurcation between “A” properties, on the one hand, and the “B” and “C” properties, on the other, and between properties in major MSAs versus those in secondary and tertiary locations with weaker tenants.

Although most retail REITs are managing their balance sheets well, the weakened operating metrics and earnings of the sector continue to generate negative ratings pressure. However, due to the steps taken by the investment-grade retail REITs over the past year, which have included but not been limited to deleveraging, increasing liquidity, laddering debt maturities and controlling expenses, ratings and outlooks should see no material change.

You must be logged in to post a comment.