A Preview of Risk Retention Effects

How will the new risk retention regulations impact the CMBS market? Fitch's Lauren Cerda weighs in.

By Alexandra Pacurar

Lauren Cerda, Senior Director at Fitch Ratings

Chicago—With less than two months to go before CMBS issuers will have to keep a portion of the loans they provide on their own balance sheets, market preparations are in full swing. The new federal rules on risk retention will be in effect starting Dec. 24, and while some issuers are testing strategies to adapt, others fear these rules could be the end of their businesses. Commercial Property Executive discussed the effects of the new regulations with Lauren Cerda, senior director at Fitch Ratings.

CPE: What are some of the short-term ramifications of the new risk retention rules on CMBS lenders?

Cerda: Given that the industry is uncertain as to how the regulators will respond to the proposed risk-retention structures being utilized by issuers, it is likely that there will be some volatility during the first quarter related to loan pricing and transaction pricing while all the parties determine the best approach.

CPE: What are some of the longer-term ramifications of the new rules?

Cerda: Further out, it is likely that the industry could see further contraction among issuers who are unable to find a risk-retention execution strategy that works for their platform.

CPE: What strategies could issuers implement in order to deal with the new risk-retention regulations?

Cerda: Issuers have tried to run a few test transactions ahead of the deadline in order to get structures fixed and documentation drafted that should lead to a smoother transition once the rules are fully in effect. It is somewhat difficult for them to really determine a final strategy at this point, since the market is waiting to hear what the regulators’ response will be.

CPE: How long do you think it will take for the market to adapt to this new lending environment and what factors will impact this timeline?

Cerda: Given that a few deals have already come to market testing the waters, it should be fairly easy to move ahead if those structures are acceptable. It’s a little more difficult to estimate the timing on how long it will take the market to stabilize in terms of loan pricing and B-piece pricing while the various risk-retention structures are finalized.

CPE: The market is already seeing a degree of volatility because of frequent changes in bond yields. Do you think these new regulations will result in more exits from the market of small or medium-size CMBS issuers?

Cerda: After first-quarter volatility, the second half of the year has seen some stabilization, and CMBS volume significantly picked up. In anticipation of the new risk-retention rules, many issuers have provided “dual track” term sheets to borrowers for loans closing either later this year or early next year that reflect the risk-retention adjustment if the loan closes past a certain date. There is some thought that if issuers are going to make borrowers pick up the increased cost, CMBS could lose additional market share to other lenders, such as insurance companies. This, in turn, could result in additional smaller shops exiting the market.

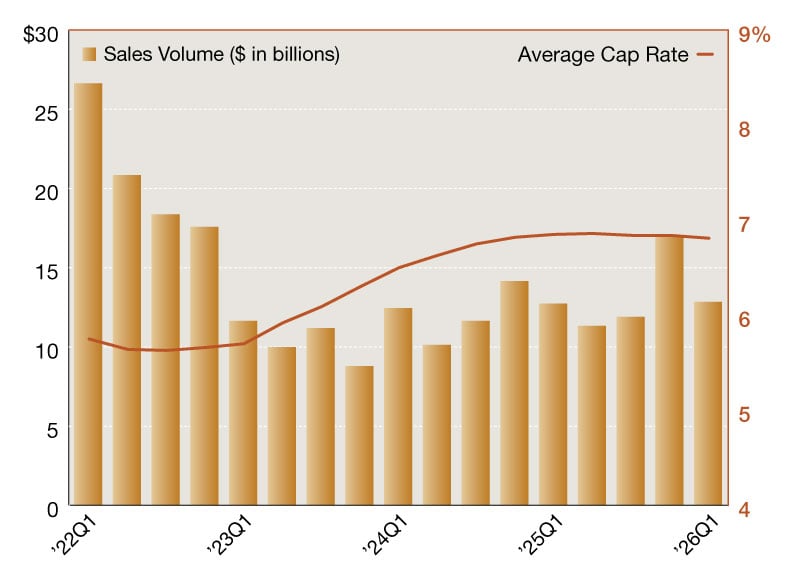

Image courtesy of Fitch Ratings

You must be logged in to post a comment.