Manufacturing’s Comeback Boosts Industrial Space Demand

What the rise of onshoring means for the sector’s market dynamics.

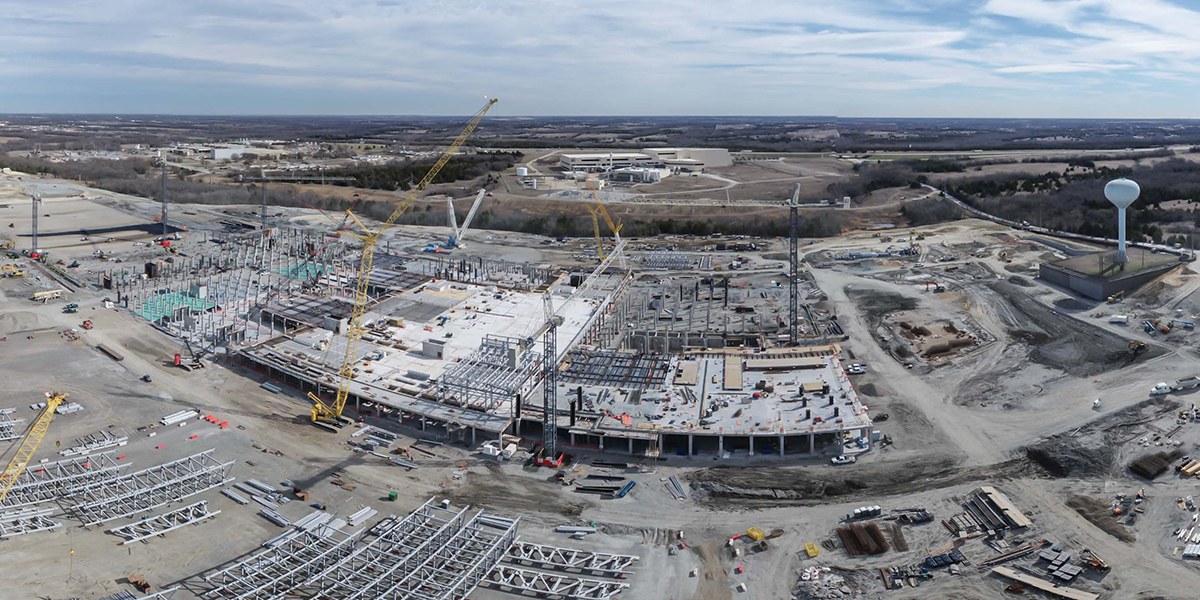

Rendering shows plans for two new leading-edge Intel processor factories in Licking County, Ohio. Announced in January 2022, the $20 billion project spans nearly 1,000 acres and is the largest single private-sector investment in Ohio history. Production may begin as soon as 2025. All images courtesy of Intel Corporation

For years, manufacturing companies have moved their production centers overseas to reduce labor and land costs and benefit shareholders. But the tide has shifted, and manufacturing is returning to North America on a large scale.

“We have seen the manufacturing sector respond to supply-chain disruptions for reasons ranging from the fallout of COVID-19 to the lack of availability of semiconductor chips,” Rene Velasquez, senior managing director of asset and property management at BKM Capital Partners, told Commercial Property Executive. “This shift has occurred rapidly, reflected by the fact that 13 new electric vehicle battery plants were announced in 2021 and are expected to be operational within the next five years,” Velasquez said. According to a report by Deloitte, transportation companies anticipate that 20 percent of freight originations from Asia will relocate to closer-proximity markets by 2025.

Pandemic lockdowns in China led to a global chip shortage and shone a bright light on U.S. dependence on Chinese chipmakers, Valesquez noted. “This dependence has created a massive trickle-down effect since semiconductor chips are used in everything from computers and smartphones to cars, microwaves and health-care devices.” Delivery time lagged and transportation costs soared; the cost of shipping a container from China to the U.S. rose some 200 percent during the pandemic.

The new globalization

While onshoring to the states long seemed to be an expensive and cumbersome task, the idea became a necessary step for many manufacturers. “The combination of various conditions for this movement (reshoring) to gain a whole new ethos happened very quickly,” Barry LePatner, founder of LePatner & Associates and a longtime real estate and construction consultant, told Commercial Property Executive. “People realized that moving production lines closer to the United States, or even Europe, would alleviate the snarls and complexities of the global supply chain.”

The reasons for shortening the distance between manufacturers and customers are numerous. Reshoring creates an increase in local e-commerce, shortens the delivery times for materials and produces thousands of jobs. Numerous manufacturing companies have already announced a shift to onshoring their operations. Last year Intel released plans to build semiconductor chip factories in Ohio and Arizona, Texas Instruments launched a $30 billion project in Texas and Taiwan Semiconductor Manufacturing Co. started two facilities in Arizona. All told, more than 75 companies have announced onshoring plans.

“Based on these announcements, we estimate demand for nearly 500 million square feet of space, including both manufacturing and related supplier networks,” said Matthew Rand, senior vice president of research and analytics at Link Logistics. He expects electric vehicle and semiconductor manufacturers to lead the resurgence.

“While the move for electric vehicles has been driven by the need to produce vehicles close to end users, the move for semiconductors has been driven by more strategic reasons, such as tax incentives and geopolitical tensions that are encouraging companies to produce chips domestically,” Rand said. On a smaller scale, manufacturing of both industrial and consumer is starting to move back to the U.S, he noted.

Texas Instruments’ $30 billion facility in Sherman, Texas, is under construction. Image courtesy of Texas Instruments

Wanted: manufacturing sites

As more companies re-shore, the opportunities for industrial real estate locations outside of major markets increases. The effects of a national supply chain turning regional could mean that more manufacturing tenants will look for sites adjacent to population centers and in infill locations.

“Infill locations are and will continue to be in high demand as they support a critical component of the modern supply chain: the ability to move product quickly with the shortest delivery times to the consumer,” said Velasquez. Infill locations often benefit from the presence of light industrial facilities as well as the location-optimization requirement, which has increased the value of properties with lower clear heights.

The dramatic increase in onshoring “has led to a significant increase in demand for warehouse and industrial spaces that don’t necessarily have traditional clear heights,” said Lee Brodsky, CEO of BEB Capital. “Companies are using these spaces both for manufacturing and storage purposes to help with the onshoring process.”

However, some infill locations are likely to remain difficult to find and expensive to develop, in part because of their appeal for onshoring manufacturers. Therefore, those CRE markets may also see more big-box space development in last-mile urban hubs and alternative markets. “Less than 3 percent of the 500 million square feet of industrial space that will be built this year will be small- or mid-bay product, while the vast majority will be big-box space,” Velasquez noted.

These spaces could be built in a variety of locations, including markets in the Southeast, the Midwest and Texas, which are generally well-suited to future manufacturing demand, according to Rand. “We continue to see new facilities popping up along the ‘battery belt,’ which stretches from Michigan down through Kentucky and Tennessee to the Carolinas and Georgia,” he told CPE.

Being close to transportation infrastructure to reduce delivery time is critical. Other key elements that play into location decisions include existing manufacturing activity, labor availability, living costs, tax incentives and manufacturing grants, said Rand. “Semiconductor manufacturers are also looking for areas with access to universities with STEM programs and competitive electric rates,” he noted.

Last-mile urban hubs, can offer savings of up to 50 percent of greenhouse gas emissions compared to less densely developed locations, Velasquez explained, and also reduce transportation costs.

Decision factors

In addition to location, a huge consideration in site decisions is the availability and cost of power. It was a key factor in BEB Capital’s recent acquisition of 9 Fairfield Blvd., a 32,745-square-foot industrial property in Wallingford, Conn. Because the city has its own electrical grid, energy costs are about one-third lower than for many other sites in Connecticut and the Northeast.

Automation, supply chain management, cloud computing and artificial intelligence technologies do much to alleviate labor shortages and improve efficiency. “The warehouse automation market is expected to grow by 1.5 times to $37.6 billion by 2025,” Velasquez noted. “Automation solutions, which are already common in large fulfillment centers (e.g., Amazon, Walmart, Target), are now being customized to accommodate smaller buildings.” Automation also yields savings that offset higher development costs for urban-core facilities, which are closer to customers and generate growing demand for light industrial space.

Automation technologies and modern practices, such as 3D printing, are transforming traditional manufacturing processes and permitting far smaller footprints. Production that once required 500,000 square feet now needs only 10,000 square feet, Velasquez noted.

As less space becomes required by manufacturing tenants, flexibly zoned sites are becoming more popular. Light-industrial properties offer manufacturers the option to locate warehousing and manufacturing and office functions in a single unit. Multi-tenant assets now often also offer enough space.

Texas Instruments’ $30 billion facility in Sherman, Texas, is under construction. Image courtesy of Texas Instruments

Ripple effects

Increased demand for manufacturing space, no matter the location or size of the facility, directly correlates to more demand for other kinds of space. Industrial and CRE companies alike will need more room to deliver equipment, building materials or other needs of manufacturers, LePatner told CPE. Also in the mix are office, retail and other commercial property types that support manufacturers and their workers.

“We anticipate that supplying and supporting (the manufacturing support network) and other new manufacturing plants will drive greater demand for mining, manufacturing, warehousing and distribution space, which is often composed of vendors found within the multi-tenant light industrial space,” said Velasquez.

That demand, partially brought about by reshoring, is pushing industrial vacancy down and prices up. Industrial rents are up 6.3 percent nationally year-over-year, according to a recent CommercialEdge report. Last year also posted a record for industrial space deliveries, with more than 450 million square feet added nationally. New space is expected to be quickly absorbed by new tenant signings from the growing ecosystem of suppliers following large manufacturers into the market.

These ecosystems are especially large around automotive manufacturers, Rand observed. “For example, when BMW began producing cars in Spartanburg, S.C., in the mid-1990s, suppliers followed to place production for important components close to BMW’s assembly plant,” Rand recalled. “Today, Mercedes-Benz, Volvo, Michelin and Magna operate in South Carolina.” A similar trend of increased industrial demand ensued in Austin, Texas, after Tesla announced plans for the Giga Texas plant in 2020.

New ecosystems won’t be created by every manufacturer, however. “Semiconductor production is relatively insulated, and most new plants will be equipped to handle almost all needs internally,” said Rand. “There will be minimal spillover impact for uses such as storing raw materials, including silicon, and specialized construction for building new sites.”

As the network of manufacturing suppliers continues to grow, the industry is feeling the pressure to develop and build accordingly. Manufacturers are in the process of vetting properties’ power potential, workforce capabilities, load capacities, zoning requirements and quality of life, while commercial real estate developers and investors are continuing to scout adjacent opportunities.

You must be logged in to post a comment.