CBRE Panel: Clearer Skies, But Office Still Cloudy

While short-term hurdles remain, the CRE sector appears poised for long-term gains.

Panelists speaking at CBRE Investment Management’s second press luncheon expressed positive sentiments around commercial real estate finance, investment and development going into the second half of the year. At the forefront of their predictions and priorities were trends around interest rates, infrastructure and sustainability initiatives.

What’s in, what’s out in CRE investment

Kicking off the conference, Wei Luo, the firm’s global associate research director, predicted an interest rate cut later this year, adding to an “encouraging” macroeconomic environment that will warm up investor sentiments. Luo welcomed the increased certainty, given both the volatility of the Fed’s repeated rate hikes last year that took place with the backdrop of decades-high inflation. “Imagine if your phone signal is unstable, and repeatedly goes on and off. That is how I felt forecasting over the last three years,” Luo said.

As for the immediate effects of these positive sentiments, Luo foresees increasingly accessible credit for new investments, alongside narrowing price gaps and valuation increases in multifamily and logistics properties, the businesses’ biggest investment darlings.

Kim Hourihan, the company’s chief investment officer, shares these perspectives on the ground, anticipating an “asset balance,” as increasingly promising sectors present themselves, while others fade more into the background. Here, it is not only the buildings themselves that are important, but the infrastructure needed to power and maintain them, coupled with how they are powered. “It’s not the old-world oil and gas, but the next generation: data centers, last mile (logistics) and cell towers,” Hourihan explained.

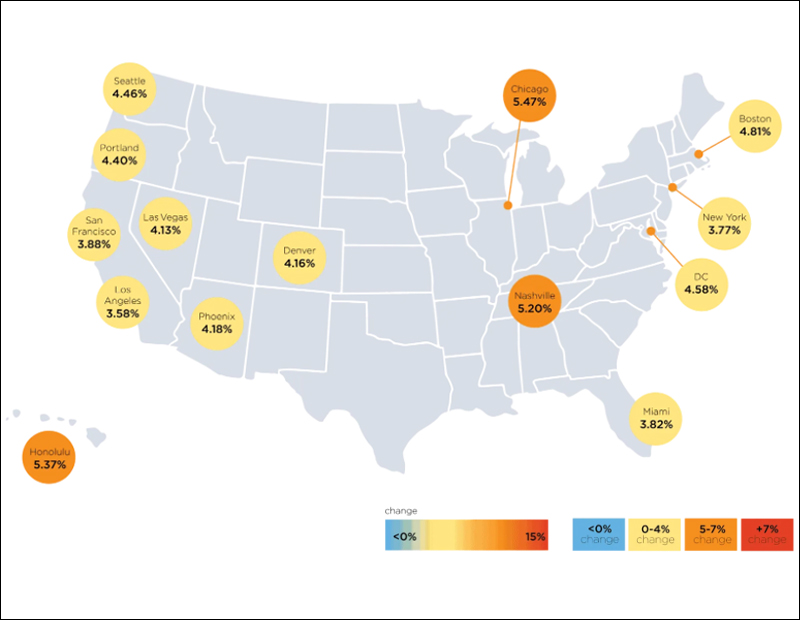

READ ALSO: CBRE Tentpole Report: Future-Proofing the Urban Core

Where the positive sentiments were lacking, however, were in the office sector, which CBRE Research has recorded as hitting a record vacancy rate in the first quarter of this year. “The fundamentals are tough, and they are going to be for a while,” Hourihan noted. “It’s not dead, but it has a lot of headwinds and challenges.”

But the panelists largely viewed such trends as more of a natural evolution than a rapid, pandemic-imposed shift on stakeholders. Hourihan compared the current investment priorities with those of 2008, 2012 and 2013, noting how the firm has elected to weigh some asset classes over others. “In 2008, there was an overweight to residential, in 2012 an overweight to logistics and an underweight to office and in 2013, infrastructure was negative and real estate was positive.”

Sustainability solutions

Dovetailing with the firm’s investment priorities were panelists’ approaches toward sustainability. The product of both increasing regulations worldwide, alongside a widespread desire to innovate on this front by many of the company’s Fortune 500 and 100 clients has led to a desire to make investment more “forward-looking and future proof,” than ever before, according to Helen Gurfel, the firm’s head of sustainability and innovation.

As for how this impacts investment in practice, Gurfel pointed to infrastructure powering the industrial facilities, data centers and the like as being responsible for 80 percent of greenhouse emissions annually, necessitating a need for sustainable energy from both an investment standpoint and that of doing right by their beneficiaries.

Closed-door conversations

Many of the sentiments and predictions expressed by the panelists are the product of extensive communication with clients, and so their perspective has been instrumental in determining the firm’s next steps. Among their chief concerns have been the ability to both supply an increasingly complex built environment with the resources it needs, coupled with a mandate to decarbonize, according to Julie Ingersoll, chief investment officer of Americas Direct Real Estate Strategies.

Additionally, the firm’s clients have been racking their brains about the demographic challenges that exist alongside an ongoing manufacturing revival and widespread investor interest in the above. As an example, Ingersoll cited Columbus, Ohio, and the large-scale investment in chip fabrication and data centers going on there as necessitating the construction of more multifamily housing.

Such concerns have spilled over to the widespread adoption of artificial intelligence and its potential impacts on both employment markets and the already ailing office sector. “If we lose 25 percent of jobs, what is the downstream impact going to be on the office sector?” Ingersoll asked.

From a pure fiduciary perspective, however, the chief problem appears to be uncertainty in credit markets, given the fact that regional banks, which provided two-thirds of debt last year, remain on the sidelines as interest rates remain elevated. One highly deleterious potential impact could be toward deflated credit spreads, which Ingersoll sees as having “negative pressure on cap rates and property values.”

Still, Hourihan predicts that 2024 will be an “excellent vintage year” for CRE investment in the long-term.

You must be logged in to post a comment.