Why MOBs Are Still a Strong Bet for Investors

And how this trend is expected to continue, according to JLL’s new report.

Medical outpatient buildings are poised for double-digit growth, according to JLL’s latest research.

A surge in outpatient demand, spurred by an aging population with even greater health-care services needs and increasing disease prevalence, puts outpatient volumes in the U.S. on track to grow by 10.6 percent over the next five years.

JLL’s report indicates limited construction for purpose-built MOBs, particularly in the Sun Belt, which is an area that has resulted in steady rent growth and continued stability for investors and health systems real estate.

Technology has assisted in a continued shift from inpatient to outpatient services, making treatments less expensive, safer and less invasive.

Therefore, health systems are expanding their real estate presence and are acquiring or contracting with physician groups to add specialty services. From 2022 to 2023, 16,000 additional physicians became employees of a hospital system, and health systems accounted for 46 percent of MOB leases that JLL tracked in 2024.

Specialty providers comprised 31 percent of the MOB leases. Psychiatrists and behavioral health providers are the leading specialty segments, accounting for 18 percent of square footage.

Savills pointed out that according to Definitive Healthcare’s 2023 survey of 195 leaders among health-care provider organizations, 60 percent of respondents’ strategic goals for the next 24 months included aligning facilities and services with changing patient demand. Additionally, ambulatory health-care employment is projected to grow 12 percent through 2028.

Health-care providers offering low- to mid-acuity services increasingly consider office and retail spaces near patients or hospitals, according to JLL’s report. This move can make conversion challenging for high-acuity or resource-intensive services such as imaging.

A resilient industry

Some will find the high level of resiliency by medical outpatient buildings amid significant economic challenges somewhat surprising, Cheryl Carron, COO at JLL’s Work Dynamics Americas & president of the Healthcare Division, told Commercial Property Executive.

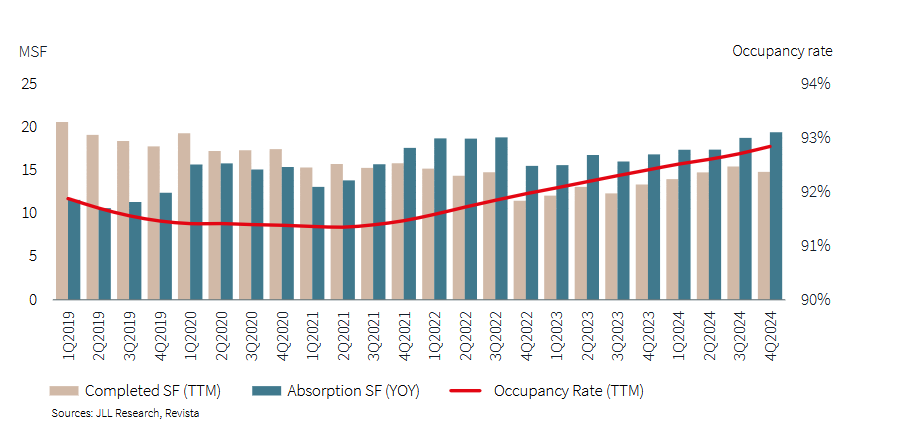

“While many real estate sectors grapple with oversupply, MOB construction remains constrained, with fourth-quarter 2024 starts at a record low of 0.8 percent of inventory,” she said.

MOBs are seeing rising occupancy rates and steady rent growth, according to JLL’s research. Absorption accelerated in the fourth quarter of 2024, surpassing 19 million square feet for the top 100 markets, and marking an increase of 15 percent from full-year 2023.

Carron said that health-care providers are seeking to expand to serve a growing need from patient populations. Still, they do so with declining Medicare and Medicaid reimbursements and slim margins, averaging just 4.9 percent in December 2024, according to the Kaufman Hall Flash Report.

“As health-care margins continue to tighten, optimizing facility efficiency has become critical for providers to maintain financial viability while meeting growing patient demand,” according to Carron.

Agentic AI creates greater efficiency

For example, artificial intelligence and other types of technology enable MOB operators to make data-driven decisions that reduce energy and maintenance costs and provide a healthier environment for patients and employees.

The Wall Street Journal reported that large language models can better understand context and provide effective agentic AI.

READ ALSO: Why the Medical Outpatient Sector Is Poised for Growth in 2025

These agents can converse with patients of human-help health-care providers when handling duties such as prescreening and scheduling, reducing clinicians’ workloads given shortages of doctors and nurses. Some of today’s AI-based tech platforms can perform about 100 actions, such as automated calls to patients after a hospital discharge.

Subdued development

MOB construction has been subdued due to developers’ need for higher returns and tenants’ desire to control expenses and elevated costs. Therefore, health-care tenants need alternative spaces due to limited medical office availability.

John Wilson, president of HSA PrimeCare, told CPE that meeting the higher demand for health-care services is challenging.

“New health-care construction has slowed over the last few years due to high construction costs and interest rates,” Wilson said. Health-care systems are also facing a shortage of physicians, he added. There are over 340 million people in the U.S., and only about 1.1 million physicians, nearly half of whom are over age 55.

Occupancy for MOBs is moving steadily higher. The rate was 92.8 percent in the fourth quarter of 2024, up from 92.4 percent one year prior.

Medical office building occupancy has steadily increased in the top U.S. metros since the second quarter of 2021, even as the development pipeline product type remains robust, according to Avison Young Principal Janet Clayton.

“Top-tier medical office buildings have experienced the steepest rent growth since 2019, whereas typical medical office buildings followed normal rental rate growth patterns during the same time,” Clayton said. “This can be attributed to a continued flight-to-quality trend across the country as tenants are willing to pay more for newly delivered products with high-quality amenities.”

MOB rents rose in 2024 from 2023, although more slowly. Top-tier properties with rents in the 90th percentile of Revista’s Top 100 markets grew at a 2.4 percent CAGR from 2019 to 2024, compared to 1.8 percent for median rates. JLL said this rate increase will be steady, not steep, because of reimbursement pressures and tight operating margins.

Aggressive expansion in South Florida

The population’s shift to the Sun Belt will produce strong growth there. However, JLL reported that strong performance in markets such as Northern New Jersey and Boston will benefit from the presence of established, growing health systems with strong brand recognition.

Four Sun Belt markets are seeing rent growth of over 3 percent: Miami; Orlando, Fla.; Austin, Texas; and Tampa, Fla.

The most significant number of new outpatient services move-ins in 2024 were in New York, and Philadelphia led all markets for MOB net absorption. Atlanta and Houston posted more than 400,000 square feet of net absorption each, and the Norfolk/Hampton Roads, Va., area saw strong absorption compared to total inventory.

One thriving Sun Belt market is South Florida, according to Colliers.

South Florida’s favorable demographic profile, coupled with the ongoing trend to provide medical care outside of a traditional hospital campus, has created a strong demand from investors and health-care providers, according to Mark Rubin, executive vice president at Colliers. He is based in its South Florida brokerage office for Palm Beach and Broward counties.

In 2019, Florida changed its Certificate of Needs regulations, which facilitated expansion in South Florida by hospital systems looking to enter the market.

“Over the past few years, we have seen Cleveland Clinic, Baptist, HCA, University of Miami, HSS, UF Shands, Tampa General, and others aggressively looking to expand their footprint in South Florida,” Rubin told CPE.

As such, medical investors have been very active in looking to purchase or develop medical office buildings to satisfy this growing demand, Rubin added. South Florida’s existing medical office inventory comprises predominantly older assets with limited availabilities.

Developers and users are alternatively seeking land or other properties (traditional office or retail) that can be developed for medical use, Rubin explained. While strong demand and limited supply exist, land and construction costs present significant headwinds for developers, and very few speculative developments are being built.

“We have had strong interest from both users and developers. With all these positive market factors resulting in a supply/demand imbalance, we believe the medical office market will continue flourishing in South Florida,” Rubin said.

Investors continue to bet on MOB

Medical office buildings remain a strong bet for investors nationwide, according to Avison Young Senior Vice President Blake Thomas.

“Interest rate changes and inflationary pressures could cause cap rates to expand further in the near term. Still, that trend is anticipated to be short-lived as demand for medical office buildings continues to show strong momentum.”

Igor Pleskov, partner & real estate practice vice chair at Saul Ewing said demographics favorable to medical office building strength would continue for some time.

“In light of development generally being slowed by interest rate and other economic pressures, I expect continued rent growth and investor enthusiasm in the market,” Pleskov told CPE.

“To the extent that macroeconomic trends become more favorable, I would anticipate more sharp increases in development. Overall, the medical office market remains strong with positive underlying fundamentals that bode well for future prospects.”

You must be logged in to post a comment.