CRE Investing: Right Move, Right Time

In an otherwise uncertain global economic environment, private commercial real estate is well positioned to achieve reasonable returns, says Situs RERC's Ken Riggs.

Ken Riggs

In games that carry risk, you have to pick the right moves at the right time to optimize your chances of winning. In investing, you have to make the right moves to maximize the return on your investment. Last year, the stock market had some ill-fated moves at the wrong times.

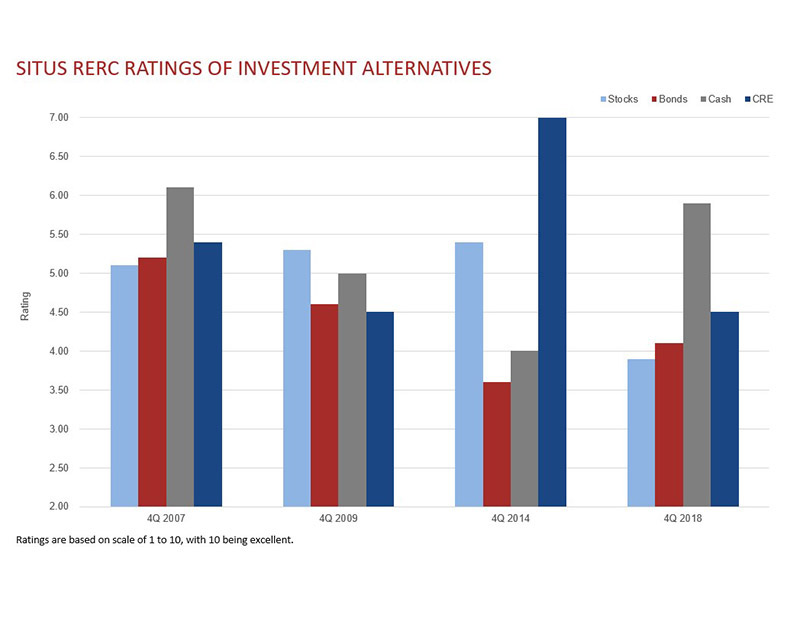

As we know, the capital markets are about diversification relative to a basket of investment alternatives and finding the move or selection that provides the best return relative to the risk of loss. The amount of risk in the market will influence the risk appetite of the market—risk on, risk off. Research by Situs RERC shows that cash was the top-rated alternative for institutional investors in 4Q 2018, which is understandable given the wildly fluctuating stock and bond markets (see the exhibit). With the economy on solid footing, CRE was the second-highest rated alternative.

Source: Situs RERC, 4Q 2018.

Although concerns about the sustainability of the overall economy, the CRE cycle’s duration and the potential of rising interest rates are putting some pressure on values, CRE remains, on a risk-adjusted basis, more attractive than stocks, cash or bonds. As we know and have come to expect, private CRE gives investors a bond-like return plus an equity upside like stocks. All signs point to institutional CRE being in a good position for the next move in the market. In an otherwise uncertain global investment environment, it is well positioned to achieve reasonable returns.

The length of any cycle―be it CRE or the economy as a whole―is not set in stone, and other factors will come into play, including interest rates. Will the Fed keep raising rates, as it did four times in 2018, or will it decide to pause? How will the government shutdown or Brexit or tariffs affect the overall economy and will any of that spill over into CRE?

It’s understandable that CRE investors want to know how they fit into the current economic environment. The U.S. economy has been moving ever upward―steadily if not always robustly―for nearly 10 years, and there are few signs of an impending recession. It’s more likely that come July 2019 we will be experiencing the longest economic expansion since the government started collecting data in the 1850s.

It is important to consider long-term value in relation to the short-term price. Are the record-high prices of CRE supported by valuations?

CRE Holding Steady

While it’s true that price and value gains are slowing down, CRE income is the strong suit in driving total returns in the near future. With strong property fundamentals, all the major property types seem to be holding their own―including retail, which has struggled in recent years due to overbuilding and the rise in e-commerce. As more consumers make online purchases, the need for distribution centers increases and demand for industrial space keeps growing. The industrial sector is expected to have the most near-term fundamentals. Many opportunities exist in the office sector, with strong demand stemming from job growth and declining vacancy. The apartment sector exhibits renewed strength, thanks in part to a continuing problem with affordability for single-family housing; however, growth in the sector is expected to moderate as supply and demand move toward equilibrium. In the hotel sector, room supply, room demand, occupancy, average daily rate and revenue per available room are at all-time highs. The office sector has been spurred by increased investment in non-major and suburban markets.

It’s far from clear when this cycle will end, and it will end one day. With other asset classes being a bit of a wild card and CRE holding steady, CRE is the best move for a diversified portfolio.

Ken Riggs, CFA, CRE, MAI, FRICS, CCIM, is president & Global Head of Situs RERC

You must be logged in to post a comment.