CRE Lenders Banking on Deal Momentum

The pickup in transactions in late 2024 is fueling optimism in 2025.

If the sentiment of commercial real estate lenders is any indication, 2025 should be a year of improving investment sales and refinancing opportunities. Banks, insurance companies, CMBS underwriters and a cadre of private credit funds are all competing (and sometimes partnering) to take advantage of a transaction market that began to show life in the second half of 2024.

“The level of interest among lenders in this environment is the strongest we’ve seen in years,” said Trey Morsbach, an executive managing director & debt platform leader for JLL. “It’s not always the case in cycles, but in this particular circumstance, the debt markets are incredibly accommodative and could be a catalyst for transaction flows.”

A recent debt fund closing by Heitman illustrates the appetite for credit investments. The firm secured more than $800 million for the vehicle—an oversubscription of $200 million—which will finance traditional and alternative properties. Similarly, SL Green Realty has gathered $500 million in commitments for a $1 billion opportunistic debt fund that will buy nonperforming loans and provide struggling owners with financing to fund leasing campaigns and capital improvements, among other strategies.

Ultimately, the growing number of bullish lenders could increase competition, translating into more aggressive pricing and better terms for borrowers, suggested Daniel Price, principal & chief investment officer at MLG Capital, a private real estate investor that has lately focused on industrial, flex, retail and multifamily properties. MLG recently launched its seventh equity fund, which is seeking to raise $400 million.

One example of more aggressive pricing is being borne in the CMBS market. Spreads on AAA bonds tightened to 92 basis points over the U.S. 10-Year Treasury in the fourth quarter last year versus 148 basis points a year earlier, according to Trepp.

“There is no shortage of debt out there,” noted Price. “Even with perceived challenges in some real estate sectors, the credit side has raised a ton of capital.”

Accelerating activity

Arguably, the biggest change in the market has been the return of banks, which after several quarters of uncertainty, are in a better position to make loans amid an increase in deposits and commercial property mortgage payoffs, according to James Millon, president of U.S. debt & structure finance with CBRE.

Meanwhile, rising annuity sales are providing insurance companies with additional cash. The companies are lending some of those funds directly to borrowers and are funneling some to property credit funds for indirect lending, added Michael Lavipour, head of lending for investment management firm Affinius Capital.

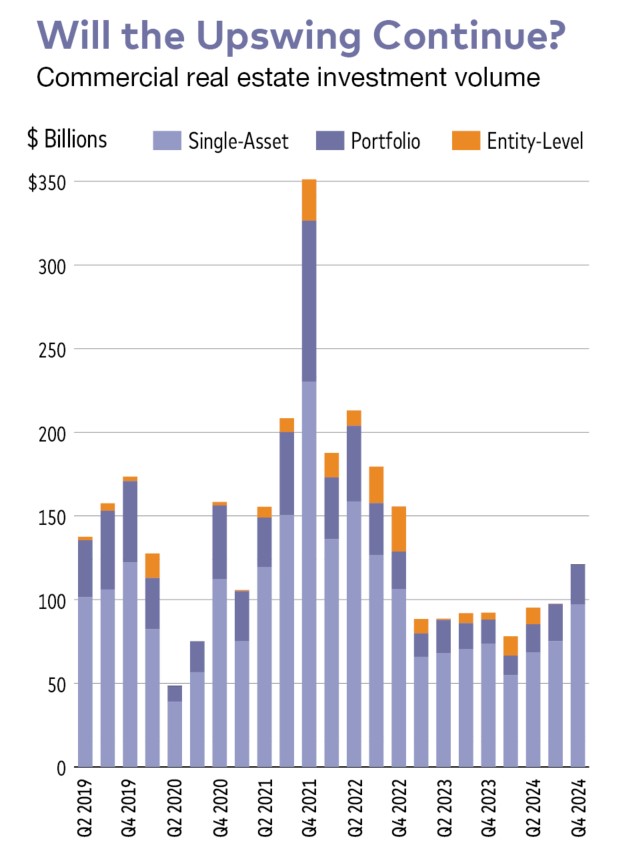

Together, banks and life insurance companies provided nearly three-quarters of all commercial property loans in the fourth quarter of 2024, a year-over-year increase of about 8 percentage points, according to CBRE. The brokerage also reported that buyers and sellers of office, retail and industrial assets executed sales totaling $67.1 billion that quarter, a year-over-year increase of 24 percent.

The increase in deals occurred on the heels of an interest rate environment that momentarily improved in the second half of 2024 as well as capitulation to the idea that interest rates weren’t going to drastically improve, observers said.

At the same time, loans and extensions are coming to term or entering an adjustable-rate period, requiring sellers to make decisions, shared Dillon Freeman, a senior commercial loan officer at Fidelity Bancorp Funding.

“Acquisition folks at family offices and other investors we work with have been pounding the pavement and making offers on tons of properties with no traction,” commented Freeman. “But recently, several of them have told me that they’re under contract for their first deal in two years. Sellers realize that they’re not going to get some sort of amazing interest rate.”

Green shoots in office

The industrial and office sectors experienced the biggest nonresidential investment activity in the fourth quarter, up 27.8 percent and 35.3 percent, respectively, according to CBRE data. The uptick in office coincided with a rebound in CMBS issuances, which exceeded $100 billion in 2024, nearly triple the securitizations in 2023, Trepp reported.

The momentum carried over into this year. CMBS issuances totaled $7.87 billion in January—a year-over-year increase of 40 percent—and nearly $9 billion through Valentine’s Day, according to Trepp.

Observers are quick to point out that most office properties remain out of favor. The uptick in office deals in many cases represented a bounce off of the investment sales bottom—and potentially the bottom of valuations—than it did a full embrace of the sector.

“There are some green shoots in office, as we knew there would be,” observed Millon. “But we need to see leases materialize and demonstrate that corporate occupiers are committed for the long term.”

Time to expand

While multitenant industrial assets account for a large slice of CBRE’s nonmultifamily capital markets opportunities, noted Millon, debt providers want to diversify into shopping centers and hospitality assets, which have experienced fundamental improvement since the pandemic lockdowns.

As part of that trend, data centers leased by major investment-grade tenants have also become a preferred asset class, said Lavipour. Just as they are doing with other large financings, banks are taking small syndicated positions in data center loans of around 10 or 20 percent, he commented. Still, the amount of debt chasing the properties has made it difficult for some lenders to justify participation in the deals.

“We haven’t seen data centers as a great credit opportunity—they feel a little overbought,” explained Lavipour, who is also on Affinius Capital’s investment committee for credit and equity products. “But we love data centers on the equity side.”

Regulation speedbump

Despite their return to the market, banks face a potential stumbling block when Basel III Endgame takes hold, which is scheduled to occur in July. The bank-strengthening rules would require institutions to significantly raise their capital reserves and take other risk-mitigating measures.

Although regulators have said that the proposed regulations could change, some banks are already moving away from direct commercial real estate lending and instead are acting as warehouse capital providers, said Lavipour. (Banks are also discovering the benefits of providing “back leverage” to debt funds.)

In the long run, the tightening regulations could drive more borrowers to debt funds and other alternative lenders, the proposal’s critics contend.

Indeed, banks already have largely stepped back from making construction loans, which is giving credit houses like BGO more access to the deals, observed Abbe Franchot Borok, a managing director & head of U.S. debt with the firm. As part of the alternative asset management division of Sun Life, BGO also sees a larger opportunity to make bridge loans to value-add investors, she added.

“The biggest headwind in the market has been a lack of transactions. But as volatility subsides, there are going to be opportunities in asset classes that until now have been on the sidelines.”

You must be logged in to post a comment.