Fed Rate Hike Ahead. What’s in It for CRE?

PGIM, Berkadia, Green Street, Moody's and others weigh in.

Federal Reserve Chairman Jerome Powell speaks at the June 14 press briefing. Screenshot of Federal Reserve livestream by Gabriel Frank

Experts across commercial real estate widely predict another 25-basis-point increase in interest rates at the Federal Reserve Open Markets Committee’s next meeting on July 26, which would bring the funds rate up to 5.25 to 5.5 percent. In turn, its impact on deal making, as well as effects on various commercial real estate sectors remain significant, contributing to sharp decreases in property values, lending and transaction volumes as well as ever more strict underwriting standards. At the same time, the economy’s relative resilience is an indicator of an eventual future of post-pandemic business.

Stubbornly focused

The expected increase, following last month’s pause, is slated to take place as the economy continuously cools, with headline inflation slowing to 3.1 percent and core inflation dropping to 4.8, their respective lowest since June and September of 2022. Despite the Fed’s incremental successes in reducing core inflation, it has still raised its projections for 2023’s peak funds rate to range from 5.5 to 5.75 percent, implying at least two more rate hikes before the end of the year.

Additionally, persistent strength in the nation’s job market has complicated the data further, with the unemployment rate falling to 3.6 percent in June, an almost 50-year low. Over that same period, wage growth ticked up to 5.7 percent, a 10-basis-point increase from April, according to the U.S. Bureau of Labor Statistics.

Despite the relative economic resiliency, the Fed’s options remain both difficult and limited, especially as its sole objective for the moment is to reduce inflation to 2 percent. Taking the totality of the data into account, John Maurer, senior managing director & head of Portfolio Management for EverWest Real Estate Investors, said: “Persistently high core inflation, coupled with the continued high labor employment rates, make it likely that the Fed will raise the rate by 25 basis points.”

Others see the labor market as an even sharper thorn in the Fed’s side, with higher wages contributing to a stubbornly high inflation rate. “We have a labor market that has been shrugging off a higher-rate environment, and all of this factors into the Fed’s decision to raise at least one more time,” observed Josh Bodin, senior vice president of Securities Trading at Berkadia.

Lending lethargy

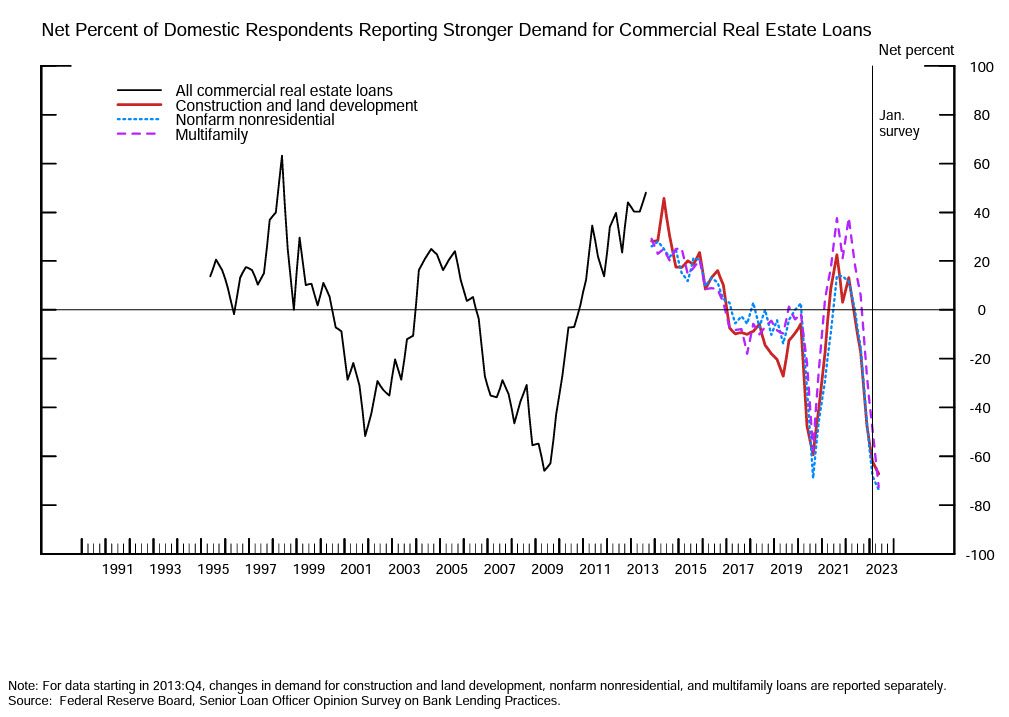

At present, lending across commercial real estate remains scarce, and barriers to entry stay stringent. There is not so much a shortage of actual capital to deploy on part of industry lenders, but inaccessible costs, made further worse by the high federal funds rate. “The key impediment to transaction volumes has not been the availability of debt, but the high cost of debt,” explained Harsh Hemnani, an analyst at Green Street.

A chart depicting the ongoing demand for new commercial real estate loans. Graph and data courtesy of the U.S. Federal Reserve

In turn, another rate hike would exacerbate the above, and reduce demand and dealmaking volumes even further. According to CBRE’s Lending Momentum Index, total loan closings nationwide have declined by 33 percent since the fourth quarter of 2022, equally attributable to inflation, as well as the repeatedly increased rates. “(It) would likely further increase costs of capital for market participants and dampen demand for loans,” Hemnani added.

The actual act of lending remains varied and largely contingent upon anticipated future market stability. Alongside inflation, key metrics that industry experts have been looking toward are five- and 10-year treasury rates, the stability of which could lead to more favorable underwriting, loan to value ratios and narrower bid-ask spreads. “Transaction volumes have been and will continue to be depressed until the markets perceive that capital markets in general and the 10-year treasury in particular have stabilized,” predicted Dori Nolan, senior vice president of Institutional Solutions at Berkadia.

READ ALSO: After Rate Hike Pause, CPE 100 Are Staying the Course

For existing loans, investors should keep an eye on maturities, particularly for assets imminently approaching a need for them. “Maturing loans with less than 8 percent yield and significant lease rollover risk are subject to higher credit risk,” noted Caglar Demir, an associate director of research at Moody’s Analytics.

What both the newer and ongoing struggles have resulted in is an environment of declining property values, where buyers “(expecting) lower prices and higher cap rates,” at the same time lenders “remain hesitant to realize losses unless they are forced to sell,” according to Hemnani.

Varying predictions

For the deals that do end up closing, the lenders’ priorities remain assets in sectors with strong, reliable long-term cash flows, and these priorities do not show any sign of changing in the near future. “Lenders will continue to focus on cash flow and debt serviceability, and will remain highly selective, but can be highly competitive for deals they like,” Henri Vuong, head of Real Estate Debt Investment Research at PGIM Real Estate, told CPE.

Consequently, Vuong sees more tech-focused commercial assets, such as data centers as attracting the most attention, especially as mainstream investors express interest in allocating capital to the assets. “Of the newer sectors, data centers are expected to benefit from the technological tailwind and adoption of AI,” Voung said.

Maurer attested to this trend directly, detailing his firm’s prioritization of “well-priced seaport industrial assets,” that are purchased in all-cash transactions, as well as select grocery-anchored retail properties, which have remained in high demand from institutional investors.

Conversely, sectors such as office, that are encountering extant, long-term hurdles and high vacancy rates have a dim outlook, even optimistically. “For office loans, there is almost no debt capital available in the market today. For trophy assets with long-term leases, office borrowers may find a loan priced in the 6 percent range,” Maurer detailed.

These fundamentals, alongside tanking property valuations, have led some to have dire predictions for the sector. Office not only has to deal with all of the above, but a widespread preference on the part of tenants to not actually work within the spaces themselves. “As much as 40 percent of the core of retail and office corridors in the nation’s cities could be rendered obsolete,” predicted Doug Ressler, manager of business intelligence at Yardi Matrix. “An estimated $800 billion worth of real estate could be wiped out,” he added.

A light at the end of the tunnel?

Depending on the economy’s performance through the rest of the year and into 2024, a resumption of higher transaction volumes, across the industry could be horizon. Key markers to look for are on the scope, scale and severity of a potential or ongoing recession, as well as an eventual reduction of interest rates themselves, once the Fed rate reaches its peak. If the outlook and performance trend positively, particularly for treasury rates, Nolan believes “the flood gates of capital will begin to open again.”

Similarly, others view the recent data itself as positive indicators, highlighting a relatively healthy economy in the face of larger struggles. “Based on our value projection—except for office—all other primary sectors including multifamily, retail and industrial will revert back to pre-pandemic value growth around 2024,” Demir predicted.

What all the involved parties need is certainty, the primary motivator for positive dealmaking sentiments. “If the Fed raises further but signals that is the last of this tightening cycle, then it would reduce uncertainty in the market and encourage transactions,” Vuong said.

You must be logged in to post a comment.