2026 Green Building Outlook: From Policy to Proof

Rules are tightening, financing is adapting and everyone wants results. Find out how sustainability will turn measurable.

As cities shift from goal-setting to enforcement and investors demand clear results, the commercial real estate industry is moving toward a new era of green building standards—one where broad climate pledges evolve into verifiable performances.

Financing is already lining up around this new expectation, and investor benchmarks are being redesigned to reward what owners can document. Many experts describe 2026 as the year when the industry enters the “proof phase,” in which the success of sustainability efforts will be measured not by intent but by results. Those who can demonstrate measurable reductions in both operational and embodied carbon will be in a stronger position with lenders, tenants and regulators alike going forward.

Local Law 97 in New York City, BERDO 2.0 in Boston, and Washington, D.C.’s Building Energy Performance Standards (BEPS) are among the first to test how owners will adapt. Each program sets baseline emissions caps, benchmarking protocols, and phased penalty schedules that escalate over the decade.

Policy & regulations: from targets to timelines

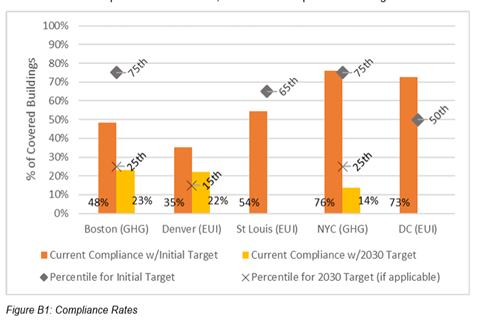

New York’s Local Law 97 moved through its inaugural reporting year with a clear emphasis on outreach over punishment. The city’s Department of Buildings spent 2025 pushing owners to start acting rather than racing to levy fines. Out of roughly 23,000 covered properties, about 94 percent of owners are now “engaged” with the city—either filed, extended or working with DOB staff on a pathway—and no LL97 penalties have been issued as of the latest update.

The focus of this inaugural cycle was emails, letters, calls and more than 60 info sessions to pull the remaining 1,500 properties onto a manageable trajectory, according to Andrew Rudansky, press secretary at New York City’s DOB. Urban Green Council’s reading of the latest benchmarking data shows that 92 percent of NYC buildings already meet the 2024 LL97 limits.

Meanwhile, Washington, D.C., reports promising early BEPS results and has pushed deadlines to keep owners on track rather than offside. In Boston, building owners subject to BERDO are required to be transparent about their buildings’ annual energy and water consumption, and comply with building emissions standards starting this year or in 2030, depending on their size.

The Institute for Market Transformation’s national read on early building performance standards tracks with that pragmatism: Jurisdictions are using flexibility while steering owners toward durable savings. According to IMT, there are several realities that owners should plan around for 2026: Inflation and tariffs have stiffened budgets, and uncertainty around the 179D federal tax credit for retrofits which will expire next year could dampen momentum if incentives aren’t extended. The policy economics remain sound—IMT’s meta-analysis places abatement costs broadly within typical for the social cost of carbon—but owners should time scopes to capital cycles and capture incentives on the table now.

“Start with strong stakeholder engagement and outreach, it’s why New York and D.C. have seen very high early compliance,” said Alex Dews, the CEO of IMT.

Overall, 2026 is best treated as an alignment window: Declare a pathway with your jurisdiction, tune operations with retro-commissioning and controls, address targeted envelope needs, then right-size and electrify when equipment reaches end-of-life. Also, lock the incentives you plan to use before terms shift.

Standards & scoring: what changes in 2026

On the investor side, Global Real Estate Sustainability Benchmark will begin scoring embodied carbon next year. “The 2025 Standard introduced non-scored developments to elevate embodied carbon,” said Charles van Thiel, GRESB’s director of real estate. “These become scored in the 2026 standard, affecting both the performance and development components.”

The expected effect is modestly positive for operating portfolios—about 0.1 point in the performance component—and a more material headwind for development, with an average decline of 5.3 points as the new indicators bite.

“The entry point for new participants (first-year reporters) reached an all-time high, indicating that sustainability progress is occurring not only within the GRESB universe but also externally, as organizations prepare for assessment against a global standard,” according to van Thiel.

For more established participants, differentiation hinges on tenant engagement, data quality, year-over-year improvements and credible building certifications.

READ ALSO: Greenbuild Special Report: Resilience Depends on Data

One certification lens, BREEAM USA, continues to expand across the country. Certified assets are now traced in 36 states, with industrial representing roughly 64 percent. Multifamily and self storage each make up approximately 10 percent, followed by retail at 7.5 percent and office at 5.4 percent, with a growing presence of mixed-use and light manufacturing projects.

BREEAM’s 2026 emphasis is practical: Pair operational performance with whole-life-carbon work, start life-cycle assessment early enough to steer specifications—especially on materials and mechanical, electrical and plumbing systems—and mine the property-condition assessment for capex and resilience planning during the hold.

“Whether you control the ops or not, efficiency first protects value, either by lowering your costs or helping tenants manage theirs,” said Breana Wheeler, U.S. director of operations of BREEAM USA.

Financing & underwriting: Capital for carbon reduction

The capital side of green building is stabilizing. C-PACE financing has evolved from an add-on to an integrated layer of the stack, and lenders are treating it as such. Senior consents and intercreditor terms now mirror institutional norms, helped by the fact that PACE assessments are fixed-rate and non-accelerating, standard notice and cure rights apply and are on the public record, making the process more predictable as familiarity grows.

Indicative 2025–2026 C-PACE rates generally range from 5.5 percent to 8.5 percent, depending on risk, leverage and tenor. Pricing and timing are increasingly predictable: Lenders cite 45 to 60 days to close in many markets, and 60 to 90 days in New York, where local processes add steps.

Underwriting is also catching up to policy—particularly for LL97 compliance, where lenders either model potential penalties or remove them when scopes clearly avoid risk. Verification now leans on third-party construction monitoring and access to ENERGY STAR Portfolio Manager.

Deal structures are more bespoke, with custom amortization and interest-only periods aligned with construction milestones instead of one-size-fits-all terms. However, most projects still require senior-lender consent, but PACE Equity reports a growing number of deals in which it served as the primary (sole) lender, eliminating consent needs altogether.

“Pricing contracted a little bit in 2025,” shared Andrew Freter, director of originations at PACE Equity. “It still remains in the low 7 percent range. Some projects with very strong fundamentals are coming in below 7 percent.”

Demand is broadening by market and use case. PACE Equity expects continued growth in New York, Dallas, Chicago and Los Angeles, with additional expansion across the Sun Belt and Midwest, and strong momentum in hospitality as banks maintain conservative leverage. The 2025–2027 maturity wall is another tailwind. Recapitalizations to replenish interest reserves, bridge cost overruns or extend amortization were robust in 2025 and should stay that way through 2026.

On tenor and strategy, the trend appears to be toward a lower-rate environment.

“While C-PACE still carries a 30-year term in most programs, projects are increasingly using it as short- or medium-term capital to construct, complete or stabilize assets,” said Freter.

At the same time, conventional guardrails remain: Standard LTV and DSCR tests still apply, even for policy-driven retrofits.

The capital stack math is coalescing. In new construction, especially multifamily and mixed-use, a typical structure combines senior debt at 65 to 70 percent LTV, C-PACE at 25 to 30 percent and equity filling the balance, with incentives layered where available. In retrofits and repositions, particularly hospitality and office-to-residential, senior leverage usually sits at 60 to 70 percent, C-PACE at 20 to 25 percent, plus targeted credits such as ITC, 179D or local rebates. The cleanest closings align PACE and senior underwriting early, locking intercreditor terms before senior documentation finalizes to prevent timing conflicts.

“C-PACE is a flexible source of capital—from new development to retrofits—and wider understanding of that is what accelerates 2026,” described Freter.

Pairing C-PACE with tax credits and sizing the financing to credit income can make it a long-tenor bridge that returns equity sooner and simplifies senior-lender consent, according to Mike Doty, senior director of originations at Nuveen Green Capital.

On the cost-of-capital side, new green-rate programs are emerging. PACE Equity’s CIRRUS offering ties reduced C-PACE rates to higher-performing certifications. BREEAM projects can qualify through that pathway, an example of how verified sustainability performance can directly influence price.

Embodied carbon & procurement: The next frontier

If developers are looking for one high-impact, low-friction move in 2026, experts point to materials. The Rocky Mountain Institute’s guidance is unequivocal: Start with concrete.

“One of the best and most cost-effective ways you can reduce embodied carbon in your buildings is to tell your project team to use low-embodied-carbon concrete,” noted Rebecca Esau, manager with RMI’s Carbon-Free Buildings Program. “Low-carbon options can be purchased at cost or with only a marginal premium depending on mix and location.”

Market data supports that advice. Responding to a request for information from the U.S. General Services Administration, more than 80 percent of concrete manufacturers said they already produce or supply low-embodied-carbon mixes, and more than 60 percent reported having product-specific environmental product declarations (EPDs). In addition, 55 percent of more than 130 businesses said their low-carbon mixes cost about the same as conventional concrete.

RMI points to a growing signal from the Sustainable Concrete Buyers Alliance, a joint initiative of RMI and the Center for Green Market Activation. Launching with founding members Amazon, Prologis, and Meta, SCoBA aggregates procurement of low-carbon concrete attributes via a book-and-claim framework.

Nowadays, financing is starting to recognize embodied-carbon reduction directly. Colorado’s SB25-182 now allows C-PACE financing for qualifying embodied-carbon improvements—opening a low-cost, long-tenor path for materials with verifiable emissions cuts, an approach other states are also evaluating.

On the risk side, insurers are tuning products for new materials. Esau notes Zurich North America’s technical underwriting work for mass timber as a sign that coverage is adapting as low-carbon options scale.

“Low-carbon concrete is the quickest win: big volumes, mature specs and, more often than not, no cost penalty,” Esau added. “In 2026, we expect buyer alliances like SCoBA to make those choices even easier to execute at scale.”

Resilience & deep retrofits: Designing for durability

Coming out of materials and procurement, the next lever is durability. In 2026, resilience starts at the shell.

“In order of priority: air sealing, windows, insulation. I do not recommend upgrading or electrifying mechanical systems until the envelope upgrades are complete,” said Al Mitchell, Phius building scientist & certification manager.

That order of operations doesn’t just improve comfort—it changes the capex math. By right-sizing equipment after the envelope work, owners typically reduce first cost and future replacement cost, with less refrigerant at risk.

“Having done that envelope retrofit first, the heat pump we install can be significantly smaller, reducing equipment cost now and replacement cost later,” Mitchell added.

Why proof matters

Investor expectations are converging on the same operational behaviors: expand asset-level utility coverage, engage tenants and connect performance to credible certifications.

“There is substantial empirical evidence connecting GRESB Scores with occupancy, cost of capital and transaction pricing,” said van Thiel, underscoring why scores matter beyond compliance.

For 2026, that translates into practical work: better metering and QA, documented tenant programs and embodied carbon metrics folded into the same reporting rhythm as energy and water. Owners that move from median to top quartile tend to do three things consistently: deepen performance data coverage and quality, strengthen tenant engagement, and integrate embodied-carbon measurement and disclosure so the evidence trail satisfies both regulators and buyers.

The coming year provides ample room to turn compliance into operations. Cities are still offering flexibility, but they are no longer debating direction. Lenders already know which scopes clear near-term limits and how to underwrite avoided penalties. Investors are ready to score embodied carbon alongside energy and water. The owners who succeed in 2026 will read that alignment plainly: Declare a pathway, tune the building you have, use capital that buys both time and savings and maintain an evidence trail that convinces regulators and buyers alike. The work is concrete, the tools are on the table and, at least for this cycle, the window is open.

You must be logged in to post a comment.