Industrial Real Estate 2021 Expectations

In the fourth installment of our 2021 outlook series, three experts size up 2020 and identify the trends that will define the year ahead.

(Left to right) Andrew Mele, Jason Tolliver, Turner Wisehart. Images courtesy of Trammell Crow Co., Cushman & Wakefield and Colliers Food Advisory Services Group, respectively

At the beginning of 2020, the industrial market was growing at an unprecedented pace. Little did we know that the word unprecedented would define the entire year. The global health crisis challenged the U.S. economy and created uncertainties across all commercial real estate sectors.

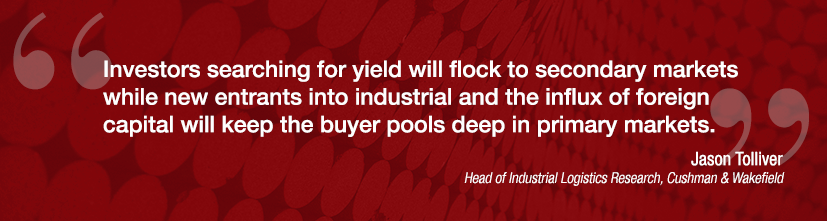

But despite the COVID-19 crisis, the industrial market remained resilient. In fact, if we were to analyze only the key commercial real estate metrics—such as absorption, vacancy, deliveries, new starts and rent growth—“it would be impossible to tell that we experienced a pandemic and the sharpest contraction of GDP since the Great Depression,” Jason Tolliver, head of industrial logistics research at Cushman & Wakefield, told Commercial Property Executive.

READ ALSO: Industrial, Data Centers Strongest Sectors in CBRE’s 2021 Forecast

Demand for industrial space surged in 2020. Third-quarter absorption was 56.2 million square feet, up 32.6 percent over the previous quarter. The overall absorption, year-to-date through the third quarter, was nearly 165 million square feet, representing a 3.3 percent growth compared to the same period in 2019, according to Colliers’ third-quarter industrial report. Additionally, a total of 252 million square feet was delivered and more than 300 million square feet was under construction as of the third quarter of 2020, Colliers found.

What’s driving growth?

The pandemic has acted as a trend accelerator for the industrial market. As shelter-in-place orders and social distancing rules were put in place, people almost instantaneously shifted to online shopping, increasing e-commerce/nonstore retail sales by 23.4 percent compared to the previous year, while food and beverage sales grew by 10.4 percent, according to Cushman & Wakefield’s third-quarter market analysis.

Colliers Food Advisory Group’s Vice President & Principal Turner Wisehart also mentioned that online grocery sales jumped from $1.2 billion in August 2019 to $7.2 billion in June 2020. “The e-grocery industry was accelerated by five to seven years in a five-to-seven-month period due to the coronavirus outbreak,” Wisehart said.

Overall, e-commerce might be credited for most of the demand in the industrial sector. “On the leasing side, e-commerce has been, by far, the largest driver of leasing velocity in most markets. Depending on the submarket, e-commerce accounts for between 25 percent and 50 percent or more of all tenant demand,” said Andrew Mele, managing director at Trammell Crow Co.

“Last year has been the year of logistics for the industrial market, with nearly all of the net occupancy growth for 2020 being carried by logistics,” noted Tolliver. Some of the markets experiencing considerable growth due to logistics include Dallas, the Pennsylvania Corridor, the Inland Empire, Atlanta and Chicago, he noticed.

Other types of industrial facilities, such as flex buildings, lost momentum due to the pandemic. According to Tolliver, leasing velocity in the flex segment has significantly slowed. On a national level, flex product occupancy was up by only 1.8 million square feet, which represents a 45 percent drop from the previous year.

Supply and demand forces

Despite the robust development pipeline throughout 2020, there’s no concern for oversupply in the near term. Due to the high demand for industrial space driven by e-commerce, new supply has actually struggled to keep up with demand, leading to significant rent increases in major distribution markets such as the Inland Empire and Northern/Central New Jersey, Mele told CPE.

According to forecasts by CBRE Economic Advisors, growth in e-commerce will drive demand for an additional 1.5 billion square feet of industrial space in the next five years or around 300 million square feet per year. Yet approximately 200 million to 250 million square feet of industrial space was delivered annually in recent years, Mele pointed out. “At this level of new supply, markets will have a difficult time keeping up with demand from e-commerce, as well as other more traditional distribution uses, for the foreseeable future.”

Mele also believes that developers might face difficulties in bringing online new product due to limited land availability and rising land costs in major markets.

“Development is growing more difficult as land becomes harder to find, and, where there is available land, some community members have begun pushing back against initial proposals for warehouse development,” he noticed. Public perception and community participation might lead to delayed approvals and entitlements, resulting in more supply constraints.

READ ALSO: E-commerce Fuels Industrial’s Unstoppable Engine

The cold storage sector is facing even more difficulties when it comes to new supply. Increased consumer demand for grocery and food products resulted in high demand for cold storage, pushing the vacancy rate below 2 percent across the U.S.

“Pre-pandemic, there was already a minimal supply of existing cold space available on the market. Now, there is almost no remaining supply because of a run on available products,” Wisehart said. Moreover, most of the available cold storage supply is outdated and in need of renovations.

In addition, developing a cold storage facility can be two-to-four times more expensive than traditional industrial buildings. Due to the high costs, cold storage is usually built-to-suit, keeping in mind the exact needs of future tenants. Nevertheless, the lack of supply prompted developers and investors to take on the risks of developing speculative cold storage, according to Wisehart. “The onset of speculative cold storage will be a defining trend in 2021,” he added.

The pandemic has fueled the growth of the industrial sector and revealed the importance of a robust supply chain, and that facilities located in or near major population centers are critical, Mele noted. He predicted a strong year for the industrial market, as retailers will continue to build out their e-commerce fulfillment platforms. Despite all this, investors should keep an eye on key indicators such as the unemployment rate and massive bankruptcies in the retail sector.

“While the acceleration of e-commerce has blunted these negative impacts, it’s reasonable to wonder about the durability of consumer spending in the face of these pressures. If consumer spending drops significantly in 2021, many expansion plans could be shelved, taking the steam out of industrial demand,” Mele concluded.

You must be logged in to post a comment.