Low Interest Rates: The Gift that Keeps on Giving!

By Marilyn Kane, President & Sean Shanahan, Senior Analyst, Iridium Capital: The recent drop in interest rates has generated a surge in buying activity in the net-lease market.

By Marilyn Kane, President & Sean Shanahan, Senior Analyst, Iridium Capital

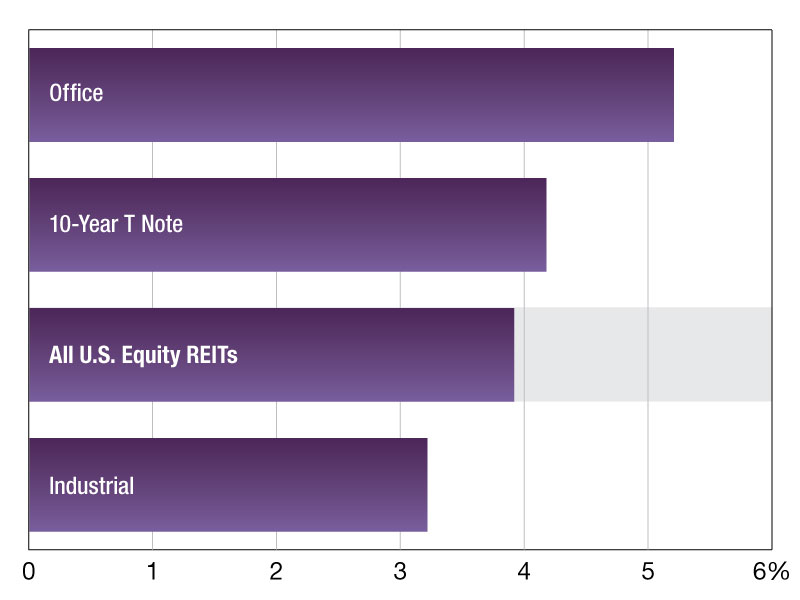

The recent drop in interest rates has generated a surge in buying activity in the Net-Lease market, leading to CAP- rate compression across all property types. Retail net-lease properties, including drugstores such as Walgreens and CVS, have always been sought by investors, and recently their annual yields have dipped to the mid-5 percent range, some of the lowest in the recent past. Discount retailers such as Dollar General and Family Dollar have also seen a surge in buying activity, leading rates to dip to the low to mid-6 percent range. Industrial net-lease properties, historically less sought after due to their high price point, cap have also seen CAP-rate compression, falling from 7 percent yields to a mid-6 percent range. Medical office and non-investment -grade net-lease properties, while generally less attractive, have also experienced increased buying thanks to the wider spread between borrowing costs and CAP rates; these properties still remain in the low 7 percent yield range.

Retail net-lease, by far the largest sector by transaction volume, has always been seen as a relatively safe real estate investment. The property is encumbered by a net lease, wherein the tenant, in addition to rent, is responsible for paying all real estate taxes, insurance, and maintenance. This structure provides the owner with a reliable and consistent cash flow with minimal responsibilities. These leases are generally guaranteed by a credit rated corporate tenant for a lease term of 15 or more years. Due to the structure, these investments operate similarly to a bond-type investment; however, they have a higher yield than similar duration bonds from the underlying tenant. In addition, these investment carry the added benefit of real estate depreciation, allowing an investor to defer ordinary income tax. Investors are also able to increase annual yield by leveraging net-lease properties, generating leveraged annual returns of 10 percent or higher depending on the tenant, location, and type of loan.

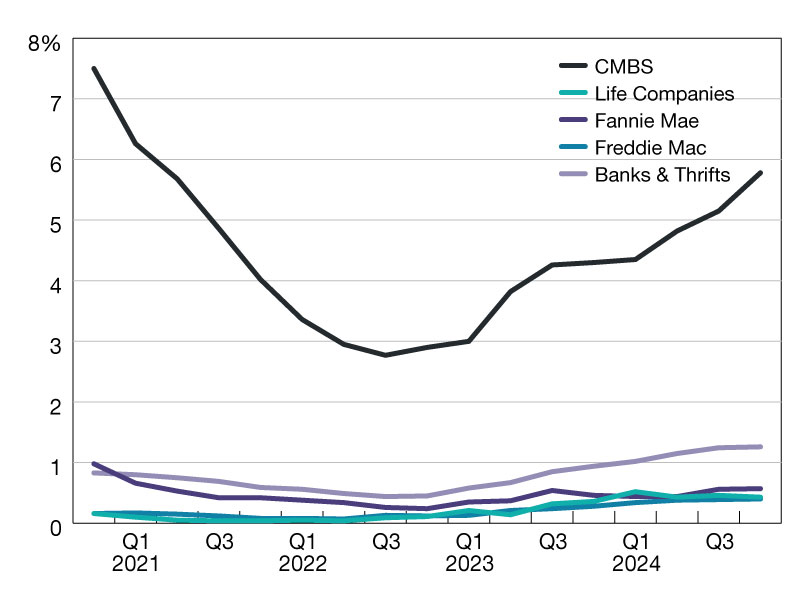

Currently, the two most sought after loan products for retail net-lease are CMBS loans and balance-sheet loans from community banks. Each loan has its own benefits and disadvantages that should be considered when deciding on property financing. CMBS loans are relatively straight forward with net-lease properties. Credit-tenant net-leased properties are generally able to be financed with loan terms of five, seven, or 10 years so long as the lease extends beyond the loan term. Borrowers are only required to guarantee the loan against bad acts, limiting personal exposure. Interest rates are generally determined with a spread above the equivalent treasury rate or swap rate, with the spread being determined by the credit strength of the underlying tenant; the higher the credit, the lower the spread. These loans generally have an interest- only period that can range from one year to the whole term of the loan, allowing for even higher cash-on cash yields for high-leverage investors. One downside to these loans is that they often have a high yield-maintenance or defeasance, which can make it costly to pre-pay the loan. An alternative to CMBS is to borrow through a community bank that lends in the geographical area in which the property is located. These loans are generally held on the bank’s balance sheet, and, because of this, they tend to have a lower interest rate. This type of loan is often limited to 65 percent LTV (loan to value), and usually will not have an interest-only component. Community bank loans are generally much more flexible in their terms than CMBS and usually have a fixed prepayment schedule rather than yield maintenance or defeasance.

Across all loan types, financing rates are near all-time lows, allowing buyers to enjoy the wide spread between purchase CAP rates and borrowing interest rates. We do not expect these rates to stay low, and just as quickly as cap rates have compressed, we expect them to rise again once interest rates begin heading up.

You must be logged in to post a comment.