US Real Estate Market Leads Globally, Despite 2023 Decline

High interest rates and pricing uncertainty continued to impact market size last year, MSCI’s latest report shows.

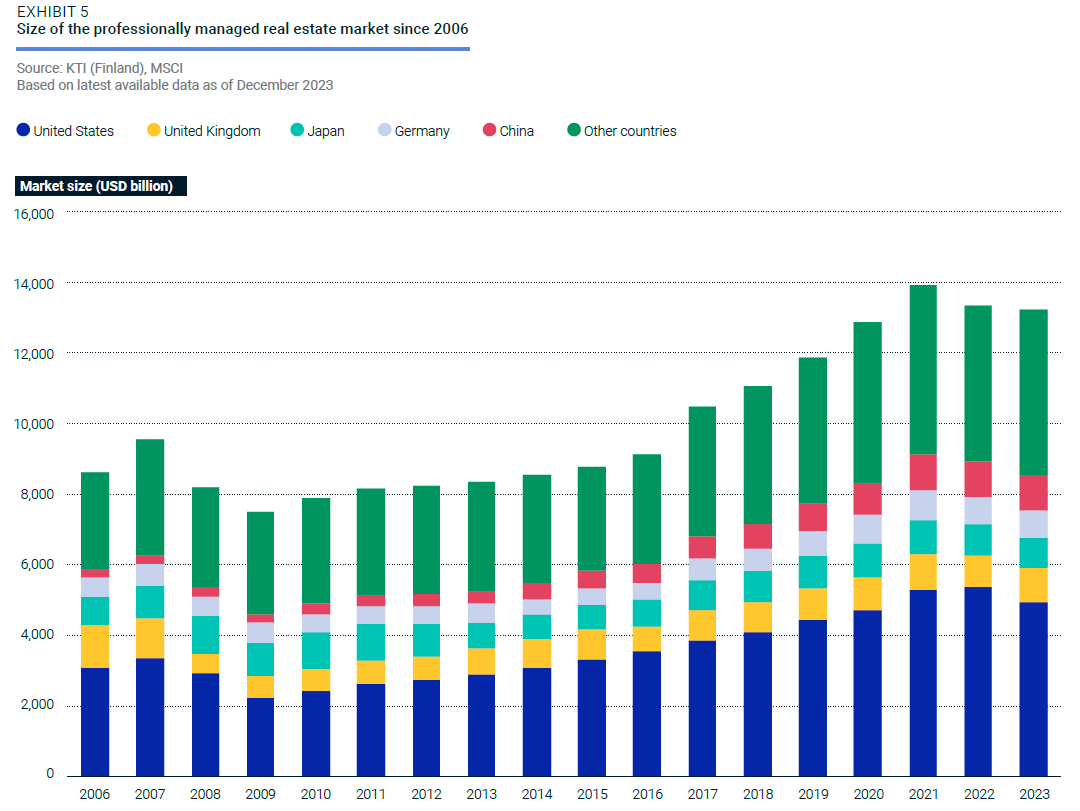

The size of the global professionally managed real estate market declined 0.9 percent, to $13.2 trillion in 2023, from $13.3 trillion in 2022, according to the latest MSCI Real Estate Market Size report. Much of that was due to continued pressure from high interest rates and pricing uncertainty.

The annual report looked at three global regions and detailed the size of 37 individual markets along with their weight in the real estate investment sector. For the first time, the report broke out the property-type composition of the global and regional markets.

“This lower pace of sales volume was not just due to potential buyers underwriting worst-case scenarios on every potential acquisition. Property owners have been loath to sell and lock in losses by matching the underwriting of potential buyers in the current market. This disconnect cements the reduced level of investment activity,” René Veerman, co-head of private capital at MSCI, stated in a foreword to the report.

READ ALSO: CRE Outlook Remains Stable Despite Headwinds

Veerman noted that commercial real estate prices began dropping in 2022, as interest rate hikes impacted the values of even favored asset classes, such as logistics. Combined with ongoing challenges to property income for office and retail post-pandemic, commercial real estate pricing is not recovering at the pace of other asset classes. In fact, Veerman stated those moves in pricing were coming at “a glacial pace” despite growth in the overall global economy.

The report states transaction volumes continued to drop in 2023, contributing to a significant reduction in the global turnover ratios. It was 5.0 percent last year, down from 8.7 percent in 2022.

U.S. market contracted from 2022 to 2023

The decline across the Americas’ market size was led by a contraction in the U.S., where it dropped from $5.5 trillion in 2022 to $4.9 trillion last year. The report found some markets increased in size in 2023, which helped prevent a larger global decline.

The Americas represented 41.5 percent of the global market size in 2023, while EMEA contributed 31.8 percent and APAC, 26.8 percent. Of the 37 markets MSCI analyzed, 29 increased in market-size weight, with the rest declining in 2023. The Americas were impacted by the weight of the U.S. in the global market size dropping to 37.5 percent from 40.3 percent in 2022.

The report cited prevailing macroeconomic challenges as contributing factors in local market size declines. However, currency movements helped the global market size last year when many currencies, including the British pound and the euro, strengthened against the U.S. dollar.

While slight—a global gain of 0.9 percent—some markets saw a bigger boost. MSCI noted the currency impact was the greatest for Switzerland, where the franc was up 9.9 precent, and Brazil, which saw an increase of 8.7 percent.

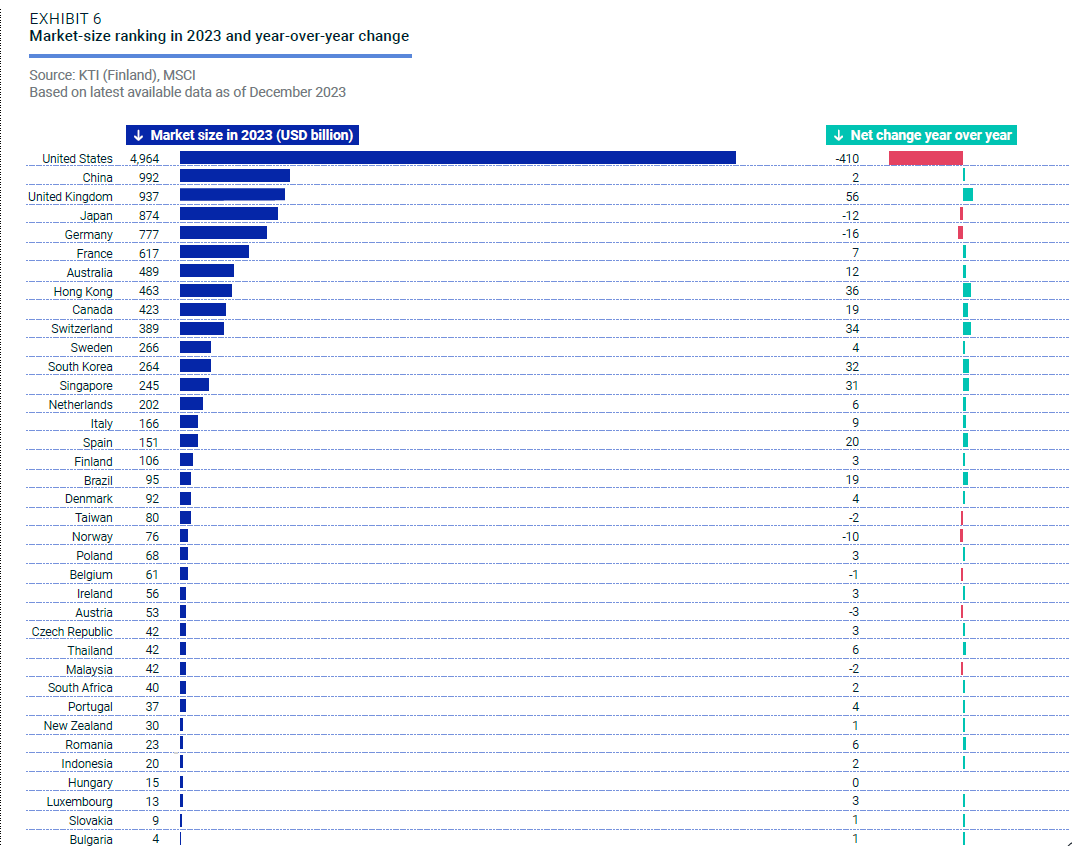

The strengthening pound helped the U.K. ($937 billion) move into the third position, behind the U.S. and China ($992 billion), in terms of market-size rankings in 2023. Japan ($874 billion) dropped to fourth place because of the sharp decline in the yen versus the U.S. dollar. Germany ($777 billion) rounded out the top five.

Office and residential remain the top sectors

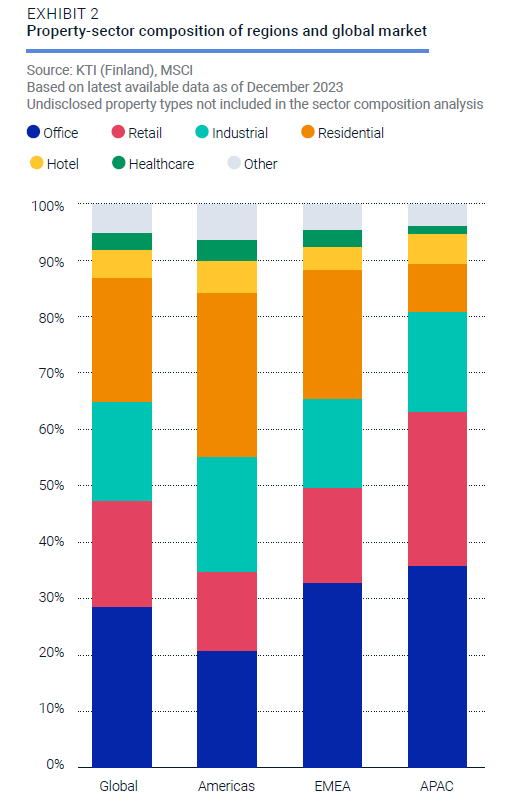

This year, MSCI analyzed seven main sectors—retail, office, industrial, health care, residential, hotel and other.

Despite challenges, the office sector continued to dominate the professionally managed market last year, with a 29 percent share of the global market. Residential followed, with 22 percent of total assets under management around the globe.

The retail and industrial sectors were 19 percent and 18 percent, respectively, with hotel and health care together representing 8 percent of the global AUM.

In the U.S., residential was the largest sector, accounting for 28 percent of the market’s AUM. In fact, the U.S. contributed more than half of the global residential AUM, according to MSCI.

The health-care and hospitality sectors represented only a combined 8 percent of the global AUM, but most of that was because of U.S. assets. The U.S. represented 53 percent of the health-care and 44 percent of the hotel AUM globally.

You must be logged in to post a comment.