What Rising Interest Rates Mean for Net Lease Investors

Competition continues to put downward pressure on cap rates—but for how long?

A volatile stock market combined with rising interest rates and inflation have yet to disturb capital pouring into net lease properties. The passive income strategy, invariably explained as a bond wrapped in real estate, provides investors with long-term credit tenants that are largely responsible for all of a property’s expenses, including real estate taxes, insurance and maintenance.

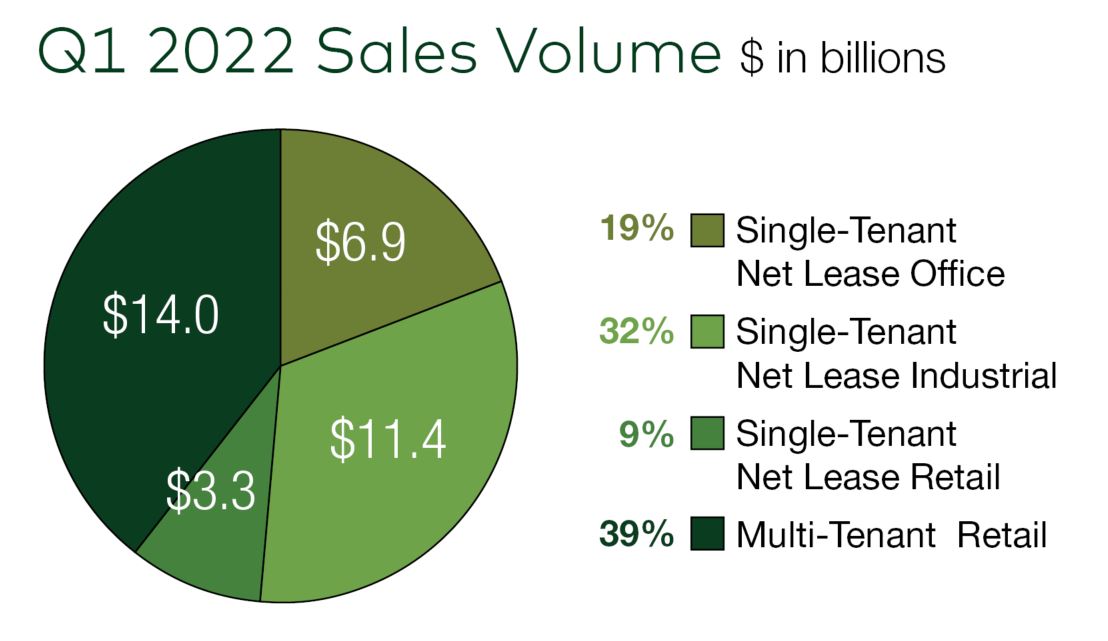

Public and private investors alike continue to plow capital into net lease assets to eek-out a return in what for the last several years has been a low yield environment. Coming out of 2021, in which industrial assets accounted for half of the $103 billion in record annual sales, single-tenant net lease deals in the first quarter of 2022 totaled nearly $21.7 billion, a year-over-year increase of 30 percent, according to Stan Johnson Co., a Tulsa, Okla.-based net lease brokerage.

READ ALSO: Why Retail Investors Are Turning to Industrial STNLs

Unsurprisingly, industrial asset sales drove the lion’s share of the first quarter business at $11.4 billion. Office and retail accounted for $6.9 billion and $3.3 billion, respectively.

Nationally, the average cap rate for net lease industrial properties dropped 17 basis points to an average of 6.6 percent in the first quarter this year from the fourth quarter last year, while office and retail cap rates experienced smaller declines to 6.7 percent and 5.75 percent, respectively, according to the Boulder Group, a net lease brokerage based in suburban Chicago.

Source: Stan Johnson Co.

For much of 2021, the benchmark 10-Year Treasury yield was below 1.5 percent, and interest rates for long-term debt were between 3 percent and 4 percent for many conventional net lease deals. That environment has dramatically changed since the end of 2021. Now interest rates are roughly 100 basis points higher, following the 10-Year bond yield’s spike of some 140 basis points to more than 2.9 percent. So far, demand for net lease properties hasn’t slowed, even following the Federal Reserve’s 50 basis point hike of the federal funds rate in early May.

“Buyers are starting to point out that interest rates are rising, but the rates aren’t full factored into the market yet,” said Jonathan Hipp, head of the U.S. Net Lease Group at Avison Young in Washington, D.C. “Quality assets with quality tenants in quality locations are still trading aggressively.”

Capitalization rates are supposed to adjust upward with such an interest rate move, although with a time lag. But observers suggest that buyers waiting for a substantial move in cap rates are likely to be disappointed.

“The correlation of interest rates and cap rates is not 100 percent, and investment demand and supply are so out of balance that cap rates won’t move as far as investors would like,” said Randy Blankstein, president of the Boulder Group. “I think there is going to be a minor adjustment to cap rates for office and retail. But industrial property cap rates may continue to compress, even in a potentially rising rate environment, because industrial remains the darling of all the sectors.”

In February, Avison Young’s Capital Markets Group represented Mesirow Realty Sale-Leaseback in its disposition of a 2.7 million-square-foot net lease warehouse in Des Moines, Iowa, for more than $325 million. Capital Square purchased the Amazon-leased property. Image courtesy of Avison Young.

Market in Transition

It wasn’t that long ago that lenders had interest rate floors because treasury yields were so low. But with the coincidental rise in treasury and interest rates, lenders and borrowers are readjusting to the market. In some cases, that means borrowers must decide whether to accept a lower cash-on-cash return or return funds to limited partners. At the same time, lenders need to deploy debt to meet their 2022 allocation targets.

“I haven’t come across any lenders that are pulling back, especially on industrial and medical office deals,” said Nicole Patel, first vice president of Four Pillars Capital, a Dallas-based mortgage banker launched by Stan Johnson in 2021. “Demand is so high right now that I can’t imagine cap rates moving. So either lenders are going to have adjust their underwriting to support current cap rates, or borrowers are going to have to be comfortable bringing more cash to the table.”

Lenders that were providing debt for 70 to 80 percent of an asset’s value a few months ago have generally dropped leverage to 60 to 70 percent, observers say. But the amount of debt a borrower receives, as well as the interest rate, also depends on location, whether the surrounding market is declining or growing economically, the strength of the sponsor, and whether a lender is over or under its allocation for a particular product, among other variables, said Ben Reinberg, CEO of Alliance Consolidated Group of Cos., a Chicago-based real estate investment firm that owns more than $350 million in medical properties.

“Lenders are hedging right now,” he said. “They want to deal with experienced borrowers who understand debt coverage requirements and don’t overleverage their properties. But for the right deal, there is real demand to finance net lease properties.”

The fact that plenty of all-cash institutional and high-net-worth individuals buyers are active in the market is likely helping to keep downward pressure on cap rates, Hipp suggested. Although they can tick up significantly between the signing of a letter of intent and closing, interest rates have yet to sour any deals on which he’s working. At the moment, he’s not too worried if they do become an issue.

“I wouldn’t advise a seller to raise his cap rate 100 basis points to make a deal with a particular buyer work, because with the amount of capital that’s driving the market, I think there’s an all-cash buyer or someone else out there who would be able to close,” he said. “If you need debt to win the competition for an asset, that might put you at a disadvantage.”

Alliance Consolidated Group of Cos. in October paid $9.25 million for a net lease healt-hcare property in Lawrenceville, Ga. Gwinnett Pediatric Partners, which operates the Atlanta Autism Center in the 12,000-square-foot building, leased back the asset for 15 years. Image courtesy of Alliance Consolidated Group of Cos.

Inflation Influence

In addition to rising interest rates, inflation is beginning to emerge as a concern for some net lease investors. Notably, rent increases built into leases may not keep up with inflation, which spiked 8.5 percent in March, the biggest annual jump in 40 years. Plus, long lease terms associated with net lease assets prevent landlords from quickly adjusting rental rates to market conditions in the same way that owners of apartments and hotels can.

Given the opportunity, net lease buyers are looking to secure healthier rent hikes going forward. Alliance Consolidated, for example, is pushing for a 3 percent annual increase in sale-leaseback transactions, and it may pay slightly more for an asset to achieve it, Reinberg said.

While some net lease agreements tie rent increases to the consumer price index, they are typically capped at around 2 percent annually. But many net leases today feature fixed annual rent increases, also of about 2 percent. Thus, continued high inflation could dramatically curb interest in the sector as the economics of deals become infeasible.

“Buyers have become hyper-focused on rent bumps and escalations in existing leases,” Blankstein said. “People want to make sure that they’re protecting the buying power of their cash flow streams.”

You must be logged in to post a comment.