Why Large Industrial Sales Are Gaining Steam

Industrial investment transactions in 2021 exceeded the prior year by 56 percent.

Adam Haefner

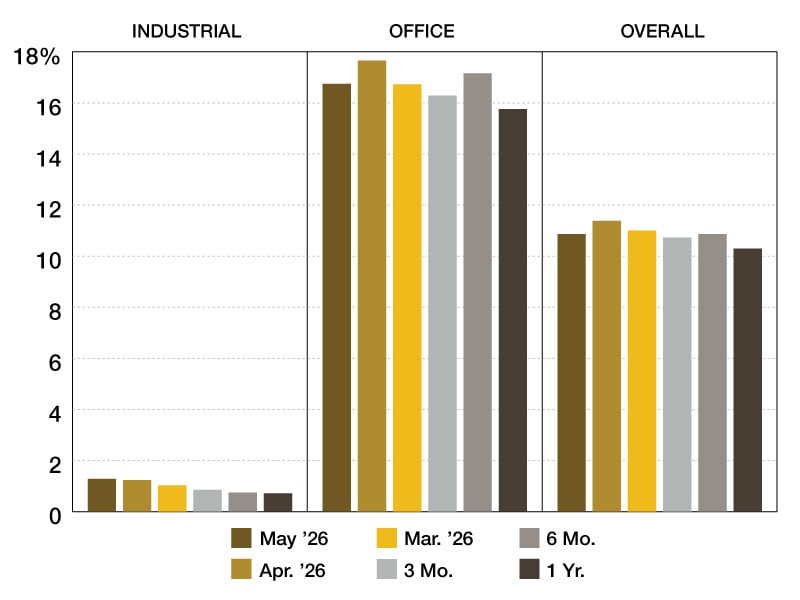

Investment sales in Chicago have remained robust over the last two years. Industrial investment activity surged to $8.9 billion in 2021, 56 percent higher than 2020. Industrial investment activity in Chicago continued to show strength in Q1 2022 with $1.6 billion, higher than Q1 2021.

Cap rates remain low, but we expect to see upward pressure because of increased interest rates. The ongoing demand for industrial product, combined with supply chain issues causing barriers to new construction, however, will keep both the vacancy rate and cap rates low in 2022. Limited supply will cause continued rent growth. So, if cap rates increase, we expect current values to be maintained.

The trend of large transactions has continued over the last 24 months. Chicago’s top buyers over the past 24 months were:

- KKR: $706.6 million and 38 properties

- BREIT: $661 million and 30 properties

- Mapletree Investments: $614.7 million and 37 properties

Chicago’s top sellers over the past 24 months were:

- Blackstone: $874.1 million and 46 properties

- Cabot Properties: $421.6 million and 17 properties

- KKR: $363.4 million and 35 properties

Maturing of the Industrial Market

Duke Realty is one of the largest industrial REITs in the country, with over 160 million square feet of buildings across the U.S. Prologis has agreed to purchase Duke Realty for $26 billion in stock, including debt. This was a 29 percent premium on their stock price at the time. This highlights the overall confidence in the market as this is one of the largest industrial transactions in the history of the sector.

Duke Realty reported 7.7 million square feet of leasing for the first quarter, leading to 99.1 percent occupancy of in-service assets and 99.4 percent for stabilized assets. Of the total 5.6 million square feet of speculative development projects delivered over the last 12 months, 5.3 million square feet of space has been fully leased. Rent growth on second-generation space was 49.2 percent on a net effective basis and 29.5 percent on a cash basis, which are record levels for the company. These factors drove up year-over-year same-property net operating income by 7.3 percent on a cash basis.

Duke Realty started eight new speculative projects, with an estimated cost of $339 million, during the quarter. Building acquisitions totaled $34 million and dispositions and joint ventures totaled $325 million for the quarter. The company has more than $800 million of development land, with more than 90 percent of it in coastal Tier One markets. The industrial sector continues to institutionalize in its ownership within the U.S. as a constant influx of consolidation offers remain in existence in the acquisition pipeline.

Two key factors contributing to higher demand is strong rent growth and the fact that lease terms are getting shorter, generally indicating that owners believe rents will continue to increase substantially. They are willing to trade the security of long-term leases for the high income growth as the space comes back to market.

Despite the recent challenges with inflation, taxes and the impacts of COVID, the Chicago industrial market has never been stronger and is not showing any signs of slowing down. Demand within the market has largely been driven by third-party logistics providers, companies in the transportation/trucking industry and tenants seeking food production or freezer/cooler space. With continued increase in demand and concerns with the supply chain, companies have shifted to increase inventory levels. This shift requires them to increase their footprint to store more inventory.

Adam Haefner is a principal in Avison Young’s Chicago office.

You must be logged in to post a comment.