Why Light Industrial Properties Will Continue to Shine

When compared to other asset types, the subsector demonstrates particular resilience, even during turbulent times.

The often-overlooked multi-tenant light industrial subsector has strong fundamentals and will remain solid in a supply-constrained environment, according to a new research study by BKM Capital Partners.

The report argues that the light industrial subsector demonstrates particular resilience, especially when compared with other property types, including larger industrial assets.

That is the case in the current high-rate, turbulent economic climate, but was also true during past crises, such as the Global Financial Crisis and the depths of the pandemic in 2020, according to BKM, which specializes in these kinds of properties.

BKM brings various data to the task of making its case for light industrial, which it defines as industrial properties smaller than 200,000 square feet, with spaces of less than 50,000 square feet. They are often used for manufacturing, but also have distribution and e-commerce tenants.

Such facilities are many times in good locations for current industrial uses, almost inadvertently, the report notes. Decades ago, many light industrial buildings were developed on the edge of cities. Since then, those urban areas have expanded, surrounding these older industrial facilities but also making them candidates for infill supply-chain networks and last-mile facilities.

Thus, such smaller industrial properties are in demand—but also supply-constrained.

The development of new light industrial assets, particularly small-bay properties, has been held back primarily by significant barriers to entry, Brian Malliet, BKM CEO & CIO, told Commercial Property Executive, adding that high land prices in prime infill locations, combined with a lack of developable land, have made new projects difficult to undertake.

“Zoning restrictions further complicate development, limiting where new industrial properties can be built,” Malliet said. “Also, the costs associated with development and financing have risen substantially, making it more challenging for developers to bring new supply to market despite strong demand. These factors have created a constrained supply environment for light industrial assets.”

Malliet said that he doesn’t anticipate a significant rebound in supply anytime soon, since the economics don’t work in the current environment.

“We’ve also seen some industrial sites being converted to multifamily developments, further reducing the already-limited inventory,” he said. “These factors make it unlikely that we’ll see a substantial increase in new supply in the near future.”

READ ALSO: Are Co-Warehousing Solutions a Game-Changer

Moreover, the report argues that history is a guide to the resilience of the subsector. Using its own light industrial portfolio of about 10 million square feet as an example, BKM reports strong leasing spreads, minimal credit loss, and high occupancy rates for the property type since 2013, when the company was founded. During the years from 2020 to the present, average occupancy for its light industrial portfolio came in at 93 percent.

Even further back, the report uses a former REIT, PS Business Parks, as a case study. The company was later acquired by Blackstone, but during the GFC, its portfolio of light industrial—that was its specialty—saw vacancies of 9.2 percent in 2010, during a particularly bad year for real estate. Overall industrial vacancies were at 13.7 percent that year.

Rents dropped for PS Business Parks during the GFC, as did everyone’s, but it was less than 10 percent. By contrast, industrial rents overall dropped by about 15 percent during the crisis.

Light industrial fundamentals

The report finds that for industrial properties smaller than 100,000 square feet—which make up about 42 percent of existing stock of U.S. industrial— the average vacancy rate in the first quarter of 2024 came in at 4 percent, a tight market indeed. For buildings between 100,000 square feet and 300,000 square feet, the rate was higher at 7.4 percent. But not as high as buildings from 500,000 square feet to 700,000 square feet, at 9 percent, or buildings larger than that, also at 9 percent vacancy.

Rents have been ballooning for the light industrial subsector as well, driven by surging demand for last-mile logistics facilities and e-commerce hubs, for which smaller buildings are well suited in many markets.

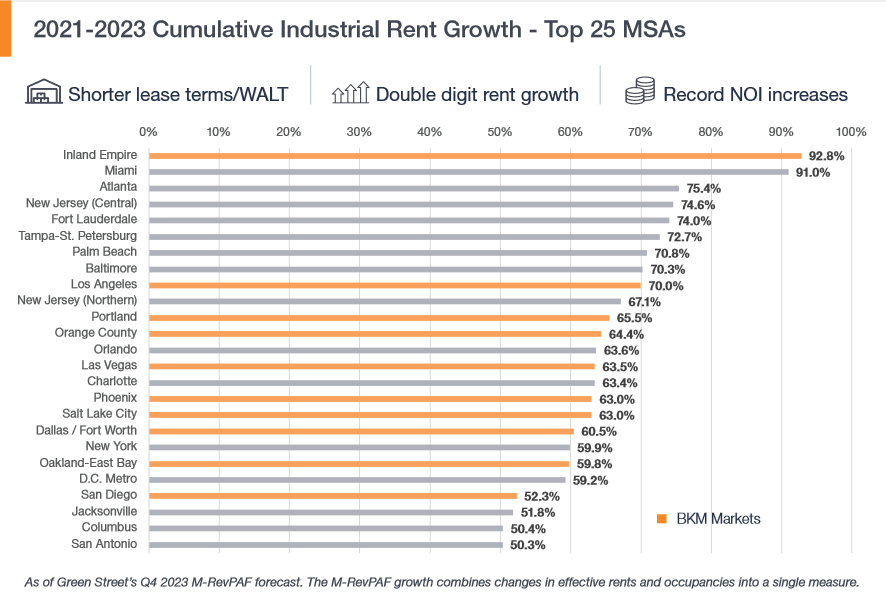

Rents for these kinds of properties have nearly doubled in the major industrial market of the Inland Empire in California, for example (up 92.8 percent between 2021 and 2023). Rents for smaller industrial properties in Los Angeles and northern New Jersey have grown 70.3 percent and 67.1 percent, respectively, during that same period.

You must be logged in to post a comment.